Thoughts of the Week

Pandora is the first woman on earth, according to Greek mythology. She was created by Zeus, after Prometheus stole the fire from heaven and gave it to mortals. Pandora was given a jar as a gift (which is erroneously referred to as a box in modern times) and was sent to earth to marry the brother of Prometheus, Epimetheus, who did not warn her about the contents. Being curious, she opened it. Evils such as greed, envy, hatred, pain, disease, hunger, poverty, war, and death were let out in the world. Nobody can blame her of her ignorance. But when it comes to geopolitics, ignorance or curiosity are catalysts for disaster. If President Trump had any clue about Greek mythology he would have been more careful before deciding to attack Iran a month ago.

It has become clear these days, that the US grossly miscalculated the risks. Vice-president Vance actually attacked Israel’s Netanyahu last week for “dragging Trump into an easy win“, according to unverified reports. What Trump thought it would be a weekend of “bing bing bing boom” as he colorfully said on public TV which would make Iran’s leadership beg for mercy, it has morphed into a serious crisis. Iran’s response to strategically attack energy targets at its neighbors and close the strait of Hormuz was not a decision made “at the spot”. They have been preparing for this and their tactics seems to be working, at least for now.

The US is being hit where it hurts most. It is not the equity market sell-off or the rise in oil prices that keeps the US administration up at night. It is the steep rise in interest rates, as a consequence of potentially higher inflation ahead, which comes at a time of unsustainably high fiscal deficits and debt for the US. According to the latest data more than 20% of the US government’s revenues are now spent to service their ballooning debt and their need for international capital to fund their deficit is greater than ever. Simply put, the US government cannot afford the 10yr yield rising to 5% or more (currently at 4.45%) and any thought of the FED cutting rates to help the situation is at the moment totally out of the question. Well done Mr. President.

Is the situation reversable ? When dealing with fanatic, theocratic regimes such as Iran’s and unpredictable, frivolous presidents such as Trump, we do not really know what the next day will bring. What we do know is that Trump has found himself in a situation which he had neither predicted nor he wants it to continue. We are sure that the US Treasury Secretary’s eyes are glued on the screen watching the yields of US debt rising, while many Republican members of Congress are already furious with the president, just seven months before the midterm elections.

No surprise that taco-Trump announced a 5-day deadline and then a 10-day extension, much like he did with tariffs, exactly one year ago. He wants a way out and everyone, including Iran, knows it. The good scenario is that Iran’s leadership wishes to keep enjoying their billions and simply throw verbal threats to the world now and then, just to keep their fanatic supporters happy. This means they will find some common ground to stop the attacks and re-open the passage of vessels, declaring “victory”. The US will present its own definition for “victory” by perhaps saying that after Khamenei’s death the “new” leadership is more cooperative and less of a threat. Then, we can continue our lives … just worrying for private credit and AI. The bad scenario is a global food, energy and financial crisis, if oil prices remain at 100$+, as the war drags on for months.

If nothing miraculously changes until tomorrow, March will be the worst month for portfolios since 2022. Global equities are down 10%, bonds have fallen in value about 4% and even Gold has cratered 20% since the start of the war, four weeks ago. A balanced portfolio in the above assets has lost more than 6% this month.

We decided to use this chaos to carefully tilt our portfolios towards higher beta. Or put in simpler words to increase our exposure to sectors that are positively correlated to economic growth, such as technology, consumer-related companies and banks, taking advantage of significantly better valuations due to the sell off. Having been cautious since February and with oil hedges in place (i.e. energy companies) as we had highlighted in this newsletter back then, we feel the time has come to assume some more risk, now that the world seems to be crumbling down. Our central scenario is that it will not.

According to the myth, Elpis (i.e. hope) remained in Pandora’s box. There are many philosophical versions of why Hesiod, the creator of the myth, chose this detail and we are not here to analyze them. But hope is all we are left with, and President Trump should perhaps take a deeper look in the box in order to find it and deliver it to the crazy new world we are living in.

Weekly highlights

March Eurozone inflation is coming up on Tuesday. Consensus expectations are for a rise to 2.7% y/y from 2% in February, almost entirely driven by the recent spike in energy prices. Annual energy inflation rate should be up about 6%, and given the weight of approximately 10% in the inflation calculation, a 0.6% jump will come just from this. On the positive side, core inflation will probably fall further to 2.3% y/y, while the important food inflation is also likely to drop by 0.1pp to 2.4% y/y.

Not a week passes by without news on private credit funds having trouble meeting redemption requests. Last week it was flagship fund managers like Apollo Global Management and Ares Management which announced that they are restricting redemptions, as these have reached a significant part of their assets under management. Retail investors who were lured into investing in these “black boxes” are now realizing that not only they cannot get their money back when they want to, but they are not even sure what the value of their investment will be when they will finally be able to liquidate. As private credit has primarily flown into AI startups in the last two years, the current credit crunch will almost certainly lead to bankruptcies in the sector.

Meta Platforms and Alphabet were found liable for causing damage to a teenager, in a landmark judicial case, in Los Angeles. Although the 3mn$ rewarded compensation is “peanuts” for the owners of Facebook, Instagram and YouTube , it could potentially open the door for a flood of lawsuits globally as a precedent has now been set. Shares of Meta fell more than 15% last week and Alphabet’s about 10%, sell-offs which partly explain Nasdaq’s weakness.

Markets’ reaction

Global equities had an interesting and volatile week. Although Europe was quick to be characterized as the main victim of the new energy shock when the first missiles were shot , it has begun outperforming the US during the last two weeks or so. Last week the S&P500 lost 2% and Nasdaq 3% , as the Euro Stoxx 50 posted marginal gains of 0.1%. Swiss stocks posted a solid performance of +2%, living up to their expectations for a “safe-haven” and most of the large caps being at the most attractive relative valuation in years. They should remain a part of any portfolio, in our view. In terms of sectors, Technology continued to be a weak link, while Energy continued higher. We decided to start taking profits in Energy, reducing our overweight which has helped a lot since the beginning of the year.

The bond market sold off again. The US 10yr yield approached the critical level of 4.50%, while the 2yr is now at almost 4% , meaning that no rate cuts are now priced in until almost the end of 2027. The German 10yr yield rose to 3.10%, which is higher than the peak in 2023, when the ECB was aggressively raising rates and inflation had skyrocketed. The 2yr yield is at 2.70%, already discounting three ECB rate hikes. We now see opportunities in high quality short-term bonds again, after being cautious on the asset class at the start of the year.

Precious metals continued to be correlated to equities. Gold lost 2% for the week , but managed to rebound from the lows of 4400$ to finish north of 4500$. Hopefully, it exhibited some of its expected hedging characteristics on Friday, when the US market was selling off.

In the foreign exchange market the EUR has been gaining against most currencies. The EURCHF has returned back at 0.9300, as the expected interest rate differential is in favor of the common currency. The EURUSD seems stuck in the range of 1.1500-1.1600 for now.

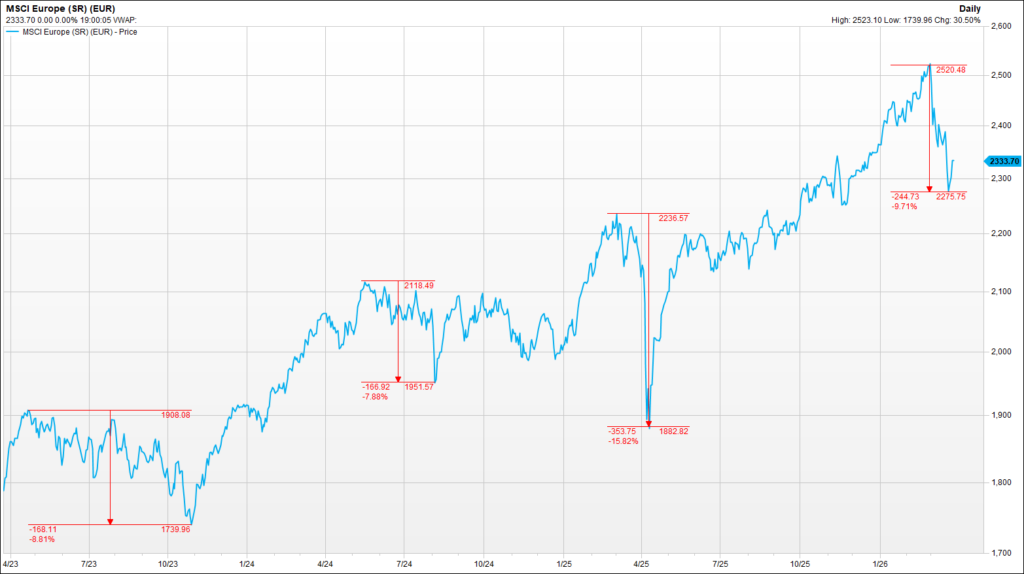

Chart of the week: A 10% correction happens every year.

Global equities have now corrected by about 10% from their very recent highs, which were back then their record levels. The 10% drop in just four weeks feels and is a lot, but it is not a rare phenomenon. The above chart shows for example the MSCI Europe equity index since 2023, and we have highlighted the periods of drawdowns that have caused concern and portfolio losses. As one can see every year there is a drop for several weeks, which can be as high as -15% as was the case last March, after Trump’s tariff announcements. Technical conditions are clearly oversold and a potential rebound in April is the most likely scenario. Whether this is a “dead cat” bounce, (i.e. a fake rally) or the beginning of a sustainable leg higher is anybody’s guess. As we have repeatedly said this year will be tough and complicated, as the war is just a catalyst for bringing equities at more reasonable valuations again, after three years of partying. Private credit troubles and AI disruption had already caused concern to investors even before the first missile struck Iran. Having said that, we remain vigilant to capture opportunities when these appear, as we did last week.

Disclaimer

- The content of this document has been produced from publicly available information as well as from internal research and rigorous efforts have been made to verify the accuracy and reasonableness of the hypotheses used. Although unlikely, omissions or errors might however happen.

- The data included in this document are based on past performances and do not constitute an indicator or a guarantee of future performances. Performances are not constant over time and can be positive or negative.

- This document is intended for informational purposes only and should not be construed as an offer or solicitation for the purchase or sale of any financial instrument and it should not be considered as investment advice. The market valuations, views, and calculations contained herein are estimates only and are subject to change without notice. Any investment decision needs to be discussed with your advisor and cannot be based only on this document.

- This document is strictly confidential and should not be distributed further without the explicit consent of Kendra Securities House SA.

- Sources : Chart: KSH / FactSet