Thoughts of the Week

Just two and a half months into the new year and they already feel like eternity. The markets kicked-off with enthusiasm for the European Renaissance and the potentially new Emerging Markets super-cycle, and quickly shifted to worries about an AI-bubble which was immediately followed by the AI-disruption scare that will kill most white collar jobs. Then banks started shaking because of the private credit woes, just to arrive to a new potential reality: a lasting energy shock that will skyrocket consumer prices and push the global economies into despair, a déjà vu just four years later. Unfortunately, we have no crystal ball to shows us which, if any, of these potential crises will be the theme of the year, or if life will return to December 2025, when things were just fine. But were they ?

On February 2nd I wrote about the market’s “entropy” (… and probably lost most of our readers), i.e. the state of equilibrium of any system in our universe, which is destined to move into a higher more chaotic level. During the recent euphoria just six weeks ago, we claimed we had reached unsustainable levels of market complacency (i.e. low entropy) and turmoil probably lies ahead which will recalibrate the system. Tremors in the markets had already appeared, with the first earthquake being the washout of precious metals. And let’s not forget that Nasdaq had already peaked late last year and the S&P500 was already flirting with negative returns even before the first strike on Iran. Investors had turned to US small caps, Europe and Emerging Markets in an effort to “ride the wave” away from AI-related bubbles or scares. The oil spike killed that trade too. But we should note at this point that the European beloved themes (infrastructure, defense etc.) had started showing signs of fatigue, even before the recent geopolitical events. The system has already started to self-cleanse from excesses and the 2nd law of thermodynamics still works !

For those of us who chose to make a living in Asset Management, our daily lives could be compared to an ER shift. It can be a nice, calm day watching Netflix and reading the news and suddenly dying patients start flocking in and chaos erupts. I should deviate at this point and say that I originally wished to become a doctor, but human pain and the fight with death were not compatible with my psyche. During my first months in the university, I saw one day the newspaper writing in huge print about the Dow Jones crashing 22%. It was October 1987, and a decision was made to plunge myself into the magical and mystical world of financial markets.

To cut a long story short, investing means accepting short or long periods of losses. But investing also means to prepare for changes in market regimes and navigating these periods to minimize capital losses, not avoid them. To this end, we had already been skeptical about the sustainability of complacency and the stretched valuations, maintaining our slightly underweight equities since last year and accepting potentially lower returns this year, if the markets went into “crazy mode”. Our sector and stock selection was skewed towards long-term growth themes, but we had already built positions in beneficiaries of potential shocks (Energy, Defensives such as Telecom and Utilities), which the market was totally ignoring back then. We had also been cautious on long-term bonds, which are sensitive to inflation but our main concern was fiscal deficits and increased borrowing by western governments.

Investors now scratch their heads to position themselves in the new, new environment. But there is probably no new, new environment. With US midterm elections coming up and the world furious with the situation, the most probable scenario is for the oil price situation to normalize, given that the last energy shock is for western governments too recent to forget. But then what ? Are we going back worrying about private credit defaults and AI, which was a month ago the “new” environment ?

We don’t want to pick a crisis. We wish to be prepared for all, until the market finds its new equilibrium state. As mentioned several times, spring will eventually bring the market lows, for now. The issue is whether the rebound will take us immediately to new highs, or this year will be one to forget about. This nobody knows.

Weekly highlights

US January inflation numbers were in-line. The CPI report, which was published, first showed that headline and core inflation remained at 2.4% and 2.5% respectively, while the PCE index, which is the FED’s inflation target came in at 2.8%, again as expected. Core PCE rose to 3.1% from 3.0% and it now stands almost 0.5% higher than a year ago, as US tariffs are finding their way into consumer prices.

US Q4 GDP was revised down to 0.7% in the second estimate, vs. the initial print of 1.4%. The BEA said the change reflected downward revisions to exports, consumer spending, government spending, and investment, while the downward revision to consumer spending was primarily due to services and especially healthcare. On the positive side, there was an upward revision to goods.

Worrisome news on private credit funds keep coming. This time it was Morgan Stanley and Cliffwater who announced withdrawal restrictions for some of their funds. The latter, who has been growing aggressively its assets by offering its funds to retail investors, said that withdrawal requests from its flagship fund reached 14% of the funds’ total assets last quarter (33bn$). The CEO of Swiss-based Partners Group also said in an interview that defaults in private credit could spike to 5% by 2027.

Markets’ reaction

Global equities had another volatile and negative week. Contrary to market wisdom which called for Europe to take the hit of Brent prices at 100$, the US equities fell more than their peers, with the S&P500 ending down 2% and Nasdaq -1.5%. Europe including the UK and Switzerland fell marginally by 0.5%, while the Euro Stoxx 50 finished the week almost flat. Local Chinese markets proved resilient, rising 0.2%, while Hang Seng shed 1%, being more correlated to Nasdaq these days. In terms of sectors, Financials (-3%) was the weakest link in the US, together with Industrials and Discretionary, while Energy (+2.5%) was the only positive sector together with Utilities. In Europe, Energy continued to rally (+7%), while Technology was also a bright spot (+2.5%).

The government bond market continued to sell off. The 10yr German bund yield approached the critical level of 3%, while the US equivalent rose to 4.30%. The nightmare of a re-acceleration of inflation because of the high oil prices has returned and charts showing similar patterns of inflation between now and the late 1970s and early 1980s have started circulating in posts and blogs, scaring traders and investors. Back then, after the initial spike and the large drop of inflation (as it happened also in 2023-2025), there was a second leg higher which brought in FED President Volcker to kill inflation and the economy at the same time.

Precious metals sold off towards the end of the week. Higher yields, higher dollar and excessive loss-making speculative positions were enough for traders to get rid of them, ahead of the weekend. Gold finished closer to 5050$, while Silver touched again the 80$ level.

The EURUSD fell below 1.1500. We had highlighted the excessive short positions on the dollar, which means that traders must buy the currency in order to close them when they are “losing their shirts” and this is what is currently happening. Whether this is a short-term blip and the EURUSD will continue its journey higher again is anybody’s guess.

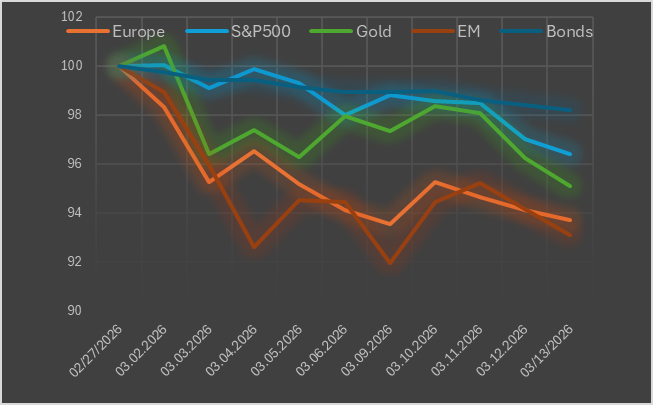

Chart of the week: No place to hide.

The above chart shows the price evolution of various asset classes since the Iran war started two weeks ago, and as one can quickly observe they are all in negative territory. Even the traditional safe-havens such as Gold (dark blue) and Government Bonds (light blue) have not been able to provide the expected protection, which means that invested portfolios did not have any support at all during this turmoil. Unfortunately precious metals have exhibited a high correlation to risky assets in the last few months, as we have noted several times, because retail traders and speculators have entered the market. These are the same that usually trade small Tech stocks or anything that has momentum. When it comes to Bonds, the inflationary pressures by higher oil prices is not friendly to them. In equities, Emerging markets (in red) and Europe (orange) have suffered the most, as they are more exposed to an energy shock, but interestingly this underperformance took place primarily during the first week and before the big spike in oil prices.

Disclaimer

- The content of this document has been produced from publicly available information as well as from internal research and rigorous efforts have been made to verify the accuracy and reasonableness of the hypotheses used. Although unlikely, omissions or errors might however happen.

- The data included in this document are based on past performances and do not constitute an indicator or a guarantee of future performances. Performances are not constant over time and can be positive or negative.

- This document is intended for informational purposes only and should not be construed as an offer or solicitation for the purchase or sale of any financial instrument and it should not be considered as investment advice. The market valuations, views, and calculations contained herein are estimates only and are subject to change without notice. Any investment decision needs to be discussed with your advisor and cannot be based only on this document.

- This document is strictly confidential and should not be distributed further without the explicit consent of Kendra Securities House SA.

- Sources : Chart: KSH/Factset, Photo: Shutterstock