Thoughts of the Week

It took a lot of back-and-forth before finally deciding to avoid any visual reference to the horrible Middle East situation. By now, your brain has already been bombarded (pun intended) by images of ballistic missiles flying in the air, piles of collapsed buildings and Iranian government officials crying in the wake of the Supreme Leader Khamenei’s death. Instead, it is better to acknowledge the fact that March is the first month of spring, but not to worry, I will not write about flowers and birds.

Spring brings more than the emotional uplift. In terms of historical data, March is not particularly friendly for US equities, as the S&P500 had 55% negative and 45% positive monthly returns in the last 30 years. But it has also been associated with market lows, before a new leg higher begins and if we take the March-May period, then 70% of the times the S&P500 has produced a positive return, with an average of +2.8%. And if we leave out the recession years, then the positive hit rate jumps to 78%. Last year, it took us into April to find a bottom, due to Trump, but thereafter the market never looked back.

The traditional “spring rebound” does not happen only by chance. For sure, seasonality helps traders and investors assume risk, but there is more to it. The Q1 corporate results are over and with them comes the end of the blackout period, during which companies cannot implement their share buybacks. Much needed corporate bids are coming back into the market. Then, most of the corporate bonuses in the US are paid in the February-March period and it is typical that a large portion of them is immediately invested in the equity market. Finally, it is the period when full-year estimates are revised by analysts, having received the Q1 results. When these have been good, as was the case this year, then there is room for full-year EPS upgrades, which is the most important catalyst for the market to move higher.

Could this time be different ? Our typical answer to such a question is No, but then again nothing appears to be working as before. I wrote about EPS upgrades being a very positive catalyst, but sentiment and market’s willingness to apply higher multiples on earnings is equally fundamental. For the readers who might not fully understand this, I will provide a simple mathematical example: If a company is expected to make 10$ per share and its P/E (i.e. the multiple on earnings) is 30, then its share price is 300$. If the market is in uncertainty mode, as it currently is, then investors are willing to pay less, for example 25 or even 20 times its very same earnings. Hence, the share price goes automatically to 250$ or 200$, without any real change in estimated profits. Hence, for the S&P500 to enjoy another spring rebound we need sentiment on Tech companies to improve again.

But the issue is that the AI-disruption fear seems to be accelerating by the day. Not a day passes without an announcement by a startup company that it is ready to replace engineers, bankers, consultants and almost everyone using a computer. On Friday, the digital payments company, Block, announced it will layoff almost 50% of its employees, as their work can be done using AI tools. The “AI war” appears to be even more daunting for markets, than the Iran situation.

Finally, moving to the fast developing situation in Iran, a major military conflict in the Middle East complicates matters even worse. Historically geopolitical events do not have lasting effects, on markets. Still, the side effects of a possible oil and freight market disruption could result in a reflex hawkish response by the central banks as higher consumer prices could become again a threat. This is especially dangerous for the US market as inflation is still around 3% and the hope has been that the FED will be cutting rates several times.

Will spring be better for US equities ? The answer will be known early summer …

Weekly highlights

Nvidia’s quarterly results were received with selling pressure. Despite the company’s solid quarterly revenues and profits as well as raising guidance for the next quarter, shares fell by more than 10% in the two trading days that followed. The main reason is the over-reliance to just a handful of companies which contribute more than 50% to its revenues but this is something we have been knowing for two years now. In the current environment of AI-induced fear, the market is questioning everything and well-established trends, companies and products are thrown under the microscope for possible disruption.

Credit spreads spiked and shares of US financials sold off, as a UK-based mortgage provider collapsed, amidst fraud allegations. This comes just one month after the collapse of First Brands Group and Tricolor Holdings in the US, which also face fraud investigations by the US authorities and caused JPMorgan’s CEO to say, back in the day, that “there are usually more cockroaches around when you see one“. Last week, he repeated his view that competitors are “doing dumb things” in pursuit of higher returns. The US high yield spreads spiked by almost 20bp and they are now 50bp higher than their record low at the end of January. We remain extremely cautious on private credit and low quality bonds.

Initial Eurozone February inflation numbers showed a mixed picture. On Tuesday March 3rd, the Eurozone composite CPI will be published and a small negative surprise could be in the cards, given last week’s country data. For now, expectations are for both headline and core inflation to have remained at previous levels, namely at 1.7% and 2.2% respectively. But on Friday, the country-level inflation data which were released were rather mixed. French CPI rose by 1.1% vs expectations for 0.7% and Spanish inflation rose by 2.5% vs expectations for 2.4%. On the positive side, Germany posted lower than expected inflation numbers for February, at 2.0% vs 2.2%.

Markets’ reaction

Global equities were positive for the week, with the exception of all US indices. Nasdaq and Russell 2000 both lost 1.2%, while the S&P500 posted a smaller loss of 0.5% helped by Energy, Staples, Healthcare and Utilities which rallied by more than 2%. Technology (-1.5%) and Financials (-2%) were at the bottom of the list. European equities were modestly higher, with its broad indices adding about 0.5%. The Swiss SMI outperformed, as the market turned defensive, especially ahead of the weekend. Energy (+3%) was strong in Europe too, confirming our positive stance of which we wrote a few weeks ago and the sector is now up almost 18% ytd.

The government bond market continued to rally in response to the geopolitical events. The US 10yr yield dropped below 4% to 3.95%, the lowest level since mid-October while the German equivalent broke down below 2.70% to reach 2.65%, the lowest level since end November. We would avoid chasing yields lower and we maintain the positions of higher duration which we talked about a few weeks ago, when 5-6yr yields were about 30bp higher.

Precious metals are attracting traders and investors, as the Iran situation is flaring up. Gold rose by 3% to touch 5300$ again and is now more than 10% higher from its recent low and just 3% below its record high. Silver broke out of its recent downtrend to touch 94$, while Platinum rose above 2350$.

The EURUSD fell to 1.1800. Geopolitical turmoil and excessive short positions are tailwinds for the dollar, at this juncture. The EURCHF fell below 0.9100 , to a new record high for the Swiss currency.

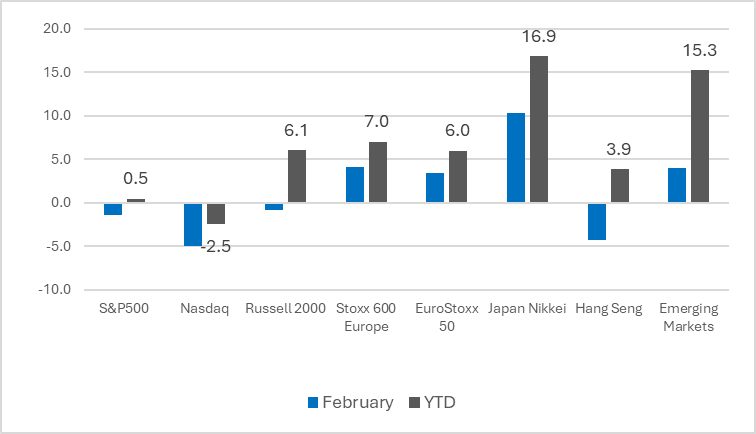

Chart of the week:

The first two months have confirmed our views, so far.

The above chart shows the performance of global indices for the month of February (in blue) and Year-to-date (in grey). The US main indices posted a negative month, while Nasdaq remains negative (-2.5%) for the year, primarily due to the Mega-cap weakness. However, the small cap index, Russell 2000, is up by 6% in the same period. The rest of the world has significantly outperformed the US, with Emerging Markets up almost 5% in February and bringing the total return to more than 15% (in USD) for the year. At the beginning of this year we wrote that Emerging Markets might have started a multi-year period of outperformance vs the US. So far this continues to prove correct, and hence we maintain our overweight exposure. Europe also had a second positive month in a row and its broad indices are up more than 6% for the year . Although two months cannot constitute a trend, the US main indices underperformance against the rest of the world seems to be accelerating, as local investors have started diversifying their holdings out of big Tech and into other markets, a trend that we have been highlighting for a few months now.

Disclaimer

- The content of this document has been produced from publicly available information as well as from internal research and rigorous efforts have been made to verify the accuracy and reasonableness of the hypotheses used. Although unlikely, omissions or errors might however happen.

- The data included in this document are based on past performances and do not constitute an indicator or a guarantee of future performances. Performances are not constant over time and can be positive or negative.

- This document is intended for informational purposes only and should not be construed as an offer or solicitation for the purchase or sale of any financial instrument and it should not be considered as investment advice. The market valuations, views, and calculations contained herein are estimates only and are subject to change without notice. Any investment decision needs to be discussed with your advisor and cannot be based only on this document.

- This document is strictly confidential and should not be distributed further without the explicit consent of Kendra Securities House SA.

- Sources : Chart: KSH/FactSet