Thoughts of the Week.

From boom to bust and then a bigger boom. Technology-related shares have been on a roller coaster since the end of last year. Fears about extreme spending on AI with no tangible profits yet were soon followed by fears of AI disrupting software and multiple other companies’ business models. Nasdaq found itself in correction territory, defined as a -10% drop from its most recent high, just a few weeks into the new year.

But then investors took notice of the explosion in memory chips’ prices due to huge demand and low supply, which made the revenues of companies like Hynix, Samsung and Micron double or triple vs last year. In a sign of the times, shares of the almost forgotten “dinosaur” Intel propelled to the highest level since the dot.com bubble in 2000. The flip side of this news is that wrong timing in expensive stocks can lead investors having to wait 25 years to get their capital back. Investors also took notice of how attractive the valuations of the likes of Alphabet, Amazon and Microsoft had become (and so did we, when we added to these positions in March and early April). The tech sector never looked back.

Fast forward to today, and Technology has accounted for all net increase in the S&P500 since the start of the Middle East conflict in late February. Other sectors have also posted decent gains such as consumer discretionary and communication services, but the biggest weights in these are also tech-related names, the likes of Amazon, Tesla, Meta and Alphabet. If we take these sectors also into account then the net contribution from Technology-related companies exceeds the combined contribution of all other sectors, many of which are still down since the start of the war.

Now the next two weeks will be crucial for the Tech-related sectors, as well as for the S&P500. All mega caps are reporting their Q1 results, but most importantly they will provide guidance for the full year. It is the time when expectations will have to be confirmed or reset (up or down). Given the recent rally, the strength of which (a 13-day winning streak) has only happened a handful of times in the last 40 years, we can conclude that this will be an important reality check for the market. Firstly, investors are keen to see whether the fears about software companies (such as Microsoft) are well founded or were exaggerated. If the German giant SAP’s solid results of last week is any guide, then we should be expecting the industry to outperform. Then, it would be important to see how much operating margins have been affected by the huge spending when Amazon, Alphabet and Meta Platforms report, as well as if there are any signs of slowing down their investment plans.

On the latter issue, last week’s news on sizeable personnel cuts by Microsoft and Meta Platforms probably point to spending being still their priority. It is probably no surprise that Meta announced its decision to cut 10% of its global workforce days before its results, and Microsoft provided a voluntary retirement scheme for 7% of its own workforce. We should be expecting to hear that spending remains robust, which is good news for the beneficiaries (electrification, data center infrastructure etc.). Last week’s ABB’s strong results and raised guidance for the year could be an early testimony for that.

Weekly highlights

Eurozone headline Purchasing Manager Index (PMI) fell to a 17-month low of 48.6 in April from 50.7 in March. This was lower than expectations for 50.1. The move back into contraction levels (below 50) was driven by services falling to a 5-year low of 47.4, from 50.2 in March. This contrasts the gains seen in Manufacturing, which continued expanding for the fourth consecutive month and at the fastest rate since last August. More worryingly, input costs increased at their fastest pace since the end of 2022, quickening across both goods and services and output price inflation hit a 3-year high.

The US Department of Justice dropped charges against FED’s Chairman Powell. This was to be expected as we are entering the final days before he will have to step down and the nominee, Mr. Kevin Warsh, will have to be endorsed by the Senate. Last week during the Senate’s Banking Committee hearing of Mr. Warsh, Republican Senator Tillis said that he will not vote for him, unless the charges against Mr. Powell are either dropped or dealt with in some way. Without Mr. Tillis’ vote the committee would have been split (12-12), if all other members voted according to the party lines, and the nomination could not pass to the Senate for the final confirmation.

Speaking of central banks, the FED and the ECB are meeting this week. No change is expected in any of these important meetings, but the press conferences should attract attention. During the last few days various ECB officials have watered down the market’s fears for runaway inflation and they have guided that the bar to raise interest rates remains high, as inflation expectations are well anchored close to 2%. The FED is in a different situation, as they have guided for rate cuts this year, a case that will have to be revisited as inflation is closer to 3% than their target of 2%.

Markets’ reaction

Global equities had a rather mixed week. The S&P500 posted small gains (+0.4%), due to Technology’s outperformance which propelled Nasdaq higher by 1.5%. The continuing momentum into Tech stocks and the lack of any sustainable solution in the Middle East were the catalysts for the significant underperformance of European equities which fell by 3%. Energy and Technology were the place to be in Europe, and especially the semiconductor stocks. Japan , which has been one of the momentum trades, also posted gains of about 2%.

The bond market was stable, with little moves on yields. The US 10yr yield traded around 4.30% and the German equivalent around 3%. The market has priced out a rate increase by the ECB on Thursday, but still about two rate hikes this year are discounted in the short-end (1-2yr), which could be an opportunity to lock in these yields , if this scenario finally does not materialize.

Precious metals fell, as the overall mood in markets was neutral to negative, except for Tech stocks. Gold lost 2% and traded as low as 4650$, while Silver is already down by almost 10% from last week’s high.

In the foreign exchange market the dollar strengthened, as oil prices recovered and the situation in Iran remains fluid. The EURUSD fell to 1.1650 after touching 1.1800 last week.

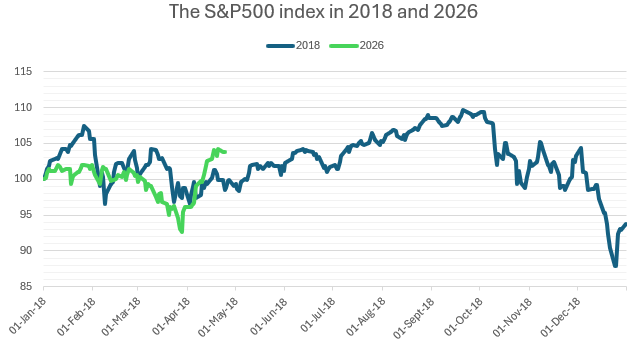

Chart of the week: What if Trump’s second year is the same as in 2018 ?

At the beginning of 2025 we had made the bold forecast that Trump’s first year as President could look like his first term, eight years ago. The similarities between 2025 and 2017 finally turned to be striking: The best performing index in 2018, among the well followed ones, was Hang Seng, and that was the case also last year when Emerging Market equities convincingly outpaced the US, after years of severe underperformance. In the foreign exchange market the dollar sold-off in 2018. And last year we had a very similar pattern, again contrary to the consensus that called for a stronger dollar the night that Trump was elected in late 2024. The above chart shows the price evolution of the S&P500 during 2018 and how it has moved until now. We can see that in both cases the year started well only to have a large correction in March/early April. Then a multi-month rebound took place which was followed by a mini crash in the fourth quarter and finally the index ended lower, despite the Christmas mini rally. Could we be in a for a repeat ? Of course the answer to this is just a toss-of-a-coin guess and the above chart is primarily for informational/entertainment purposes and not intended to base any decision on it. We will revisit this theme when December comes.

Sources : Chart: KSH / FactSet

The content of this document has been produced from publicly available information as well as from internal research and rigorous efforts have been made to verify the accuracy and reasonableness of the hypotheses used. Although unlikely, omissions or errors might however happen.

The data included in this document are based on past performances and do not constitute an indicator or a guarantee of future performances. Performances are not constant over time and can be positive or negative.

This document is intended for informational purposes only and should not be construed as an offer or solicitation for the purchase or sale of any financial instrument and it should not be considered as investment advice. The market valuations, views, and calculations contained herein are estimates only and are subject to change without notice. Any investment decision needs to be discussed with your advisor and cannot be based only on this document.

This document is strictly confidential and should not be distributed further without the explicit consent of Kendra Securities House SA.