Thoughts of the Week

Writing this newsletter on a beautiful, sunny Saturday with financial markets in a crazy party mode, what else than the iconic “Saturday Night Fever” movie can come to mind. The reference to the wild life of Tony Manero might puzzle some of our readers and reveal the writer’s age, but the fact that the movie was a major hit around the time that the Islamic Revolution took place in Iran, makes it perhaps more relevant. And here we are, fifty years later to wonder whether the recent developments in the region should be enough to make us jump on the dancing floor or start thinking about what comes next.

Most of our views have been confirmed, but as Andy Grove, founder of Intel, once famously said “Success breeds complacency, and complacency breeds failure”. Early in this year, as clouds were starting to gather above Iran, and Trump had already showed signs of brewing aggression (Venezuela, Greenland) we decided to place an overweight position in Energy stocks as a hedge and because shares were trading at very attractive valuations. Then in early March, for those who remember, we opined that spring usually comes together with the lows of equity markets and decided to cautiously increase positions in riskier segments of the market that had corrected a lot (Technology, Industrials, Banks). All these have worked nicely, but this not the time to celebrate.

Are we going to have a 2025 repeat ? It seems that Trump starts every year with a “shell bomb” which pushes the markets in correction through early/mid April, only for him to realize that he has caused unnecessary damage to his own voters. Last year equities bottomed around this time of the year and never looked back. The AI revolution and the prospect for the FED to cut interest rates were enough catalysts. Although we have a deep dislike for the cliché “This time is different“, it would probably be a mistake to simply copy-paste what worked well in the last three quarters of 2025.

Analyzing the pillars of last year’s rally, things are starting to look different. For starters, inflation has again become an issue even if there will eventually be some sort of “peace” in Middle East. Oil prices should remain elevated for at least a few months and the FED is nowhere near to cut rates. The AI revolution has been turning into a nightmare for many companies and citizens. Last week, Maine became the first state in the US to pass legislation for a moratorium on new data centers, and Georgia, Virginia and Oklahoma are preparing the same. According to the Financial Times, major projects for Microsoft, OpenAI and other tech groups are likely to miss completion dates by more than three months, according to data from SynMax, a satellite and AI analytics group, partly because of permitting hurdles. It is estimated that almost 40 per cent of projects due this year are at risk of falling behind.

Although we are happy with the market’s evolution in April, a major part of the rally was due to short covering. According to the available data, hedge funds had built massive short positions and algorithmic funds had reduced their exposure significantly as the war erupted. Being short and out of equities quickly became a “pain-trade”, and hedge funds rushed to close their short positions. Algorithmic funds only last week joined the party and started buying again, as volatility fell. All this means that normally we should not be expecting a continuation of the rally at this crazy rate. I would emphasize the word normally, because nothing is normal this year and hence, anything can happen. Last but not least the situation in Iran is still fluid.

Vigilance is still the pillar of our investment strategy, even if we are tempted by the Bee Gees song “You should be dancing” that accompanied the solo of John Travolta (Tony Manero). Hence, we decided to cut our exposure to long-duration government bonds, as the risk remains for higher interest rates and we also cut equity exposure, by selling US small capitalization companies for non-US based portfolios. This means that during this party we raised our cash balances, awaiting to see how financial markets evolve in the coming weeks and we are ready to re-invest in opportunities as these arise.

Weekly highlights

The EU is planning the biggest relaxation of its rules on corporate mergers in decades, according to the Financial Times. The European Commission will give greater weight to “innovation, investment and resilience of the internal market”, when deciding whether to sign off on deals, according to draft guidelines. If adopted by the Commission, the new policy approach would reflect a broader change in the political mood across the continent, with calls to enable more “European champions” to take on corporate giants in the US and China. “The guidelines are a break from the past,” an EU official said, calling them “an ambitious approach that reflects the realities of increasingly challenging global competition”. This is very positive for the region.

Some Wall Street banks have started trading credit default swaps (CDS) against private credit vehicles of major asset managers, according to reports. These products, which gain in value in case of defaults, began trading after S&P Global earlier this week launched the index CDX Financials, which also includes investment vehicles run by Apollo, Blackstone and Ares, as well as banks, insurers, real estate companies and other financial groups.

The IMF’s World Economic Outlook. which was released last week, devoted two chapters to the macroeconomics of defense spending. Nearly 40% out of 164 countries now spend more than 2% of GDP on defense, up from 27% in 2018. In the same report it is mentioned that since 1946, the defense spending boom in developed countries has lasted about 3 years , and spending is very front-loaded. The main reason for the sequential drop in the growth rate of defense spending has historically been the decrease in active conflicts but also the eventual reduction in social spending as fiscal positions become strained . Governments then face social/voter pressure to reduce the rate at which they are spending on defense. Currently the global % of GDP spent on defense has already risen to 2%+, the highest since early 2000. The record high since the early 50s has been 3% in the 1970s and 1980s, far less than the 5% that NATO has set as a target for 2035. This looks too far away and too high vs history, which could later be abandoned or altered. We have recently cut our exposure in defense stocks, but remain invested.

Markets’ reaction

Global equities reached new highs, propelled by the steep fall in oil prices. The spike was primarily driven by the Technology sector which helped Nasdaq spike higher by almost 7% and register a 13-day winning streak, a record since 1992. US markets clearly outperformed Europe, which posted a respectable 2% gain for the week. On a year-to-date basis, Europe still manages to slightly be ahead of the US while Emerging markets are again the clear winner with a 14% gain since the year started. The mega Tech results coming up in the next two weeks will be a test for the market or the catalyst for a new leg higher.

The bond market rallied too, as inflation fears subsided. The EUR curve moved lower by about 20bp, which confirmed our view that last week’s rates were a good entry point again, especially in the short-medium maturities. Of course, the situation will remain fragile as oil prices could remain elevated (75-85$) for long, even if a peace deal is finally achieved.

Precious metals posted a solid week, as correlation with equities is now positive. Gold rose 2% to 4830$, while the market’s darling, Silver, was the winner with a 6% jump to 83$.

In the foreign exchange market the dollar continued to sell off. The EURUSD briefly visited 1.1840 before settling down at 1.1770. The EURCHF has returned at 0.9300, which was the rate at which it spent most of 2025. Any new escalation in Iran will be positive for the dollar, again.

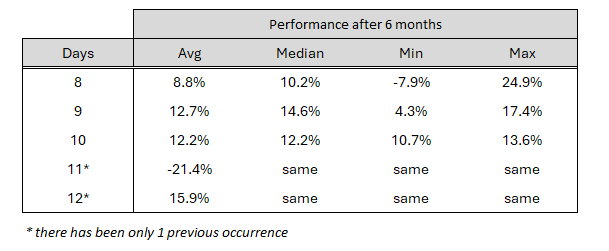

Chart of the week: What happens 6 months after such a large winning streak for Nasdaq ?

The above chart shows the performance of the Nasdaq composite index 6 months after a large winning streak (i.e. consecutive days with positive closes). As mentioned in the footnote there has only been one occurrence with 11 positive closes, and that resulted in a subsequent drop of more than 20%. Those 11 days of rally ended in November 2021 and marked the end of the 2020-2021 party, as inflation moved higher and the central banks started raising interest rates fast. The 12 days of consecutive wins also has one previous occurrence, back in July of 2009, after the financial crisis. As Nasdaq had collapsed by more than 50% into the March 2009 low, the period that followed produced a strong rebound. Looking at smaller winning streaks (8-10 days) which are somewhat more often in the last 20 years, we see that overall the market continues to do well on average, producing returns of 8-12%. This does not constitute a guarantee of higher returns; it is just for illustrational purposes and to show that a “crazy” rally does not necessarily mean that markets have topped.

Sources : Chart: KSH / FactSet

The content of this document has been produced from publicly available information as well as from internal research and rigorous efforts have been made to verify the accuracy and reasonableness of the hypotheses used. Although unlikely, omissions or errors might however happen.

The data included in this document are based on past performances and do not constitute an indicator or a guarantee of future performances. Performances are not constant over time and can be positive or negative.

This document is intended for informational purposes only and should not be construed as an offer or solicitation for the purchase or sale of any financial instrument and it should not be considered as investment advice. The market valuations, views, and calculations contained herein are estimates only and are subject to change without notice. Any investment decision needs to be discussed with your advisor and cannot be based only on this document.

This document is strictly confidential and should not be distributed further without the explicit consent of Kendra Securities House SA.