Thoughts of the Week.

Having read Aldous Huxley’s novel at the tender age of 17, when neither the internet nor the social media or AI existed, I was shocked. A future of engineered happiness through a combination of technological and pharmaceutical means, where individuality is sacrificed in the name of stability and human beings are categorized as groups A to E, was definitely not what I was imagining while getting ready to enter the world as an adult. And although it is really tempting to spend a few paragraphs of this newsletter on comparing today’s world with what the distinguished writer described almost 100 years ago, the purpose of the title is to primarily characterize the state of current global affairs and the new investment environment that has emerged.

Although cracks had been appearing, it seems that the pandemic accelerated the move into this new world. Until then, investors were surrounded by an environment which was primarily characterized by globalization, peace and stable technological innovation. Now, all these three pillars have been shaken from the ground. Yes, Brexit and (first-term) Trump had already given blows to globalization, but it was the supply chain collapse due to the lockdowns that triggered the rush to bring manufacturing “back home” and securing access to raw materials and energy. Putin had already invaded Crimea in 2014, but in 2022 he started a full-blown occupation attempt in Ukraine that has led to a relentless re-armament not seen since the cold war. It has even pushed German auto makers into thinking of getting into the defense industry (again). Lastly, the technological advances of the last six years have been parabolic, starting with working-from-home applications and infrastructure to today outsourcing software coding to AI agents.

The “previous” world was also an environment of non-existent inflation and very low or zero interest rates in the major economies. Lest we forget, Germany was borrowing money with negative interest rates for many years, or in other words, investors were lending them capital and also paid the interest to them ! All this now belongs to history. In 2022, the Bloomberg U.S. Aggregate Bond Index fell 13%, its worst year on record, taking down with it all other asset classes (equities, gold), as interest rates rose to levels last seen in the early part of this century (bond prices move inversely with yields). Four years later, bond yields have returned to the same levels as in 2022.

This “new” world has been and will continue to be characterized by higher inflation and higher yields, higher than most investors have been accustomed to in this century. And this view is not based on the recent events that have caused oil prices to spike. For starters, central banks want inflation because it means that companies’ revenues have a tailwind due to increasing consumer prices, wages are also improving and the broad economy is benefitting. The equity market is, therefore, benefitting from “good” inflation. Inflation becomes an issue when there is a sense of “losing control” as it happened in 2022/2023 and could happen now if oil prices shoot up to 150$ as few commodities analysts predict. Lastly, the sharp deterioration of government public finances in the major economies (high fiscal deficits, high debt), also a byproduct of the pandemic which was never resolved is another important reason of this new world of “permanently” higher interest rates.

Regardless of what happens in the Middle East, global yields are destined to remain elevated. The US equity market’s narrative at the end of last year was that the FED will normalize interest rates to much lower levels and bond yields will follow lower, as inflation was in the right direction and the labor market was weakening. This consensus thinking has already been proven wrong due to the military conflict’s impact on oil prices, but we should not forget that bond yields had other periods of spiking (with oil at 60$), as it happened in April of last year. Then it was due to Trump’s tariff policies and a “Sell America” mood among international investors, which not only has not abated, but Trump’s aggression has pushed even more of their creditors having second thoughts about maintaining a high exposure in US Treasuries. All this means that it is difficult to envisage much lower yields for now. In Europe, the bond market was already predicting higher yields before the war, as higher government spending on infrastructure and defense is beneficial to both growth and inflation, so there was no need for the ECB rates to stay at 2%. And lastly, Japan has been transforming itself into a “normal” country, allowing inflation to rise and allowing yields to rise with it, after decades of zero interest rates. The 250% Debt/GDP ratio of the country will eventually spook bond investors in the local government debt market, as yields rise further.

A new investment environment is under way in equities as well. And although the current headlines are again on the renewed AI-related stock party in the US, this is just noise. The underlying regime in equities seems to be changing. China appears to be grasping the opportunity to re-introduce itself. The second largest economy in the world, has turned from the provider of cheap labor, cheap products and copy-cats to a technological superpower (electric vehicles, robotics, AI etc.), but more importantly to a pillar of stability in a volatile world. It is no surprise that Emerging Markets significantly outperformed the US last year and continue to do so in 2026 until now, and the trend could continue for years to come.

In Huxley’s world-class novel, citizens were daily consuming “Soma“, a drug provided by the State and which offered vivid hallucinations, sensation of deep pleasure and moments of happiness. Investors had been having their own Soma for decades too, in the form of abundant and ultra-cheap money. In 2022, this medication was removed, and they suffered. Since 2025, desperate voices in the US (aka Trump) have been asking for the dosage to return (i.e. the FED to slush rates aggressively) and investors had already felt withdrawal symptoms, as the US equity market had essentially stalled since November of last year and then moved into correction this year, even before the start of the Iran conflict. The current AI frenzy, based on short-covering and retail investors pouring massively in 2x and 3x leverage semiconductor ETFs (according to available data) could be just a hallucination, a Soma-type moment in history, if the FED does the “unthinkable”, to raise interest rates. Stay tuned.

Weekly highlights

April inflation in the US came in hotter than expected. The headline CPI increased 0.64% on a month-to-month basis, pushed up by gasoline prices which most probably will impact May’s numbers too. The 12-month rate rose to 3.81% from 3.26% in March. The core CPI rose 0.38% m-o-m, and the 12-month rate moved up to 2.75% from 2.60%, pushed up by airfares and much higher housing inflation which however is due to recalculations from the missing October data due to the federal government shutdown.

Kevin Warsh was confirmed by the Senate as the next FED Chairman. The next step to take officially the seat is to be sworn in, which could happen this week. In the meantime, Mr. Powell will remain Chairman pro tempore. If sworn in time, Mr. Warsh’s first meeting will be in about a month, where he will will face the ex-Chairman who has decided to stay on the Board of Governors. The new Chairman is already into deep waters, as inflation is approaching 4% and the labor market has remained resilient, which means that the case for rate cuts is simply not there. At the same time, the US President who is the one who finally chose Mr. Warsh is pushing for aggressive rate cuts. And to complicate matters worse, the recently appointed ultra-dove, Mr. Miran is not there anymore and already a few voting members are contemplating a hike, not a cut.

The MSCI All World Equity Index underwent the largest rebalancing on record, in terms of number companies being added and deleted. The main regional change was the increase in the weight of Emerging Markets by approximately 0.5% to 11.5%, with more additions coming from China, India and Brazil. The difference came primarily from Europe’s weight dropping by 0.5% to about 15%, while the US remained at around 64% of the index.

A Blackrock Private Credit Fund is under investigation by the authorities, about its mark-to-market practices. According to the FT, the US Attorney’s Office for the Southern District of New York has asked information about BlackRock TCP Capital Corp, a publicly traded credit fund. Jay Clayton, head of the office, said last week: “If people are mismarking in order to generate fees, that’s always been a no-no,” speaking at a conference for the alternative assets industry. There has been growing concern among investors that the valuations of the loans to private companies have potentially been artificially inflated to boost fees and mask potential financial distress. The Blackrock Fund (TCPC) marked down the value of the loans it held in late January, writing down its assets by 19% and a separate class action complaint filed against TCPC in February alleged that it had failed to disclose “material adverse facts” about its business. The California filing said the company’s net asset value had been overstated and positive statements about its business were misleading.

Markets’ reaction

Global equities lost ground, as the S&P500 touched a new record high in the meantime. The sell-off at the end of the week brought global indices into the red, with the US still managing to outperform during this renewed AI frenzy. Nasdaq was down by only 0.1%, as European indices fell by 1.5%-2.0%. Swiss stocks managed to post gains, as the risk-off sentiment drove investors into “safety stocks”. In terms of sectors, Energy was the big gainer, advancing 4% in Europe and the US, while defensives (healthcare/consumer staples/utilities) were also positive contributors.

The bond market sold off as already mentioned. The US 10yr yield broke above 4.50% and moved to 4.57%, while the 30yr is now well established above 5%. In Europe, the UK 10yr yield rose to the highest level of the last forty years, and the German 10yr reached 3.15%, the highest in two decades. A 10yr US yield close to 5% will not be taken well by equities.

Precious metals were very volatile. The week started with an unexplainable rally of 10% for Silver, to reach above 86$, only to lose everything and more and at the end of the week to find itself to 77$. Gold moves were less muted, with a failed attempt to capture the 4’700$ level when silver was rallying and finished the week at 4’530$. Higher yields, a stronger dollar and sell-off in equities are not the best friends for Gold at the moment.

The dollar rallied as expected , given the spike in yields. The EURUSD fell to 1.1630, as short positions were closed and its next move depends almost exclusively on what happens to oil prices and hence bond yields.

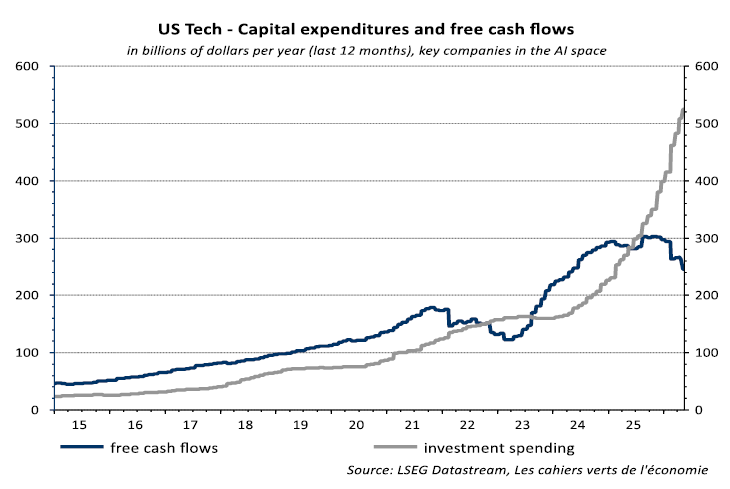

Chart of the week: US Technology, memories of early 2000s re-emerge.

The beauty of the mega US Technology companies has always been the combination of their asset-light business models and the ever-increasing cash flows that were generating. With asset-light we mean that their products were scalable on a global basis without the need of huge spending on factories, supply chains and infrastructure like most other “old economy” businesses have to. The AI revolution in 2023 has changed all that. They have become capital intensive businesses and their free cash flow generation has sharply deteriorated, as shown in the above chart. We cannot ignore the similarities with the internet bubble, when Telecom companies became the most valuable companies in the world as the internet was starting to get widely known and used. They started spending billions on internet lines and infrastructure for the coming revolution, but soon realized that the returns on these investments were not as anticipated in the beginning, because bandwidth prices collapsed as fiber supply far outpaced demand. When they stopped spending the whole ecosystem collapsed (i.e. the companies which were involved in the infrastructure chain and had borrowed heavily to ride the wave of the internet revolution). The truth is that the internet revolution did happen of course, but at a much lower price than the companies’ aggressive business plans had anticipated. AI is here to stay and will also revolutionize our corporate and personal lives. Whether the overwhelming money being spent now is going to come back as much higher revenues and profits to the companies is the trillion dollar question. The market’s answer is yes, as it was in 1999.

Sources : Chart: Cahiers Verts

The content of this document has been produced from publicly available information as well as from internal research and rigorous efforts have been made to verify the accuracy and reasonableness of the hypotheses used. Although unlikely, omissions or errors might however happen.

The data included in this document are based on past performances and do not constitute an indicator or a guarantee of future performances. Performances are not constant over time and can be positive or negative.

This document is intended for informational purposes only and should not be construed as an offer or solicitation for the purchase or sale of any financial instrument and it should not be considered as investment advice. The market valuations, views, and calculations contained herein are estimates only and are subject to change without notice. Any investment decision needs to be discussed with your advisor and cannot be based only on this document.

This document is strictly confidential and should not be distributed further without the explicit consent of Kendra Securities House SA.