Thoughts of the Week

I do not own the intellectual property of this phrase, but it perfectly fits the current period. In just a few days, European equities lost more than 6%, erasing all gains they had accumulated in the first two months of the year. The Euro Stoxx 50 index fell from its record high set on February 25th to the lowest level since end of December of last year and the German DAX is almost 10% down from its record high in a few trading sessions. The sell-off was less steep in the US, as investors and traders concentrated their selling to our region, which is the most impacted by the oil price spike and with proximity to the Middle East. The opening of the new trading week does not look good either.

March is already living up to our expectations, as historically is the month which brings capitulation and inflection points. Staying invested in a prudent way is the wise investment decision. But if you wish to sell the market, you have to do it for the right reasons. And geopolitics is never the right one, unless a full-scale nuclear war has already started and in which case, I would not even be writing this newsletter.

If oil prices were to stay at 100$+ for months, this would definitely have an impact on inflation, earnings etc. Of course, this would be a reason to recalibrate investment strategies. Then again, we cannot conceive how President Trump would wish to go to midterm elections in 8 months from today with high gasoline prices, interest rates higher and equity market crashing. Hence, a compromise between the Iranian government and Trump should be in the cards, while no regime change is in sight.

Market gyrations have become relentless. The market moved from the AI-disruption fear that cratered software companies and other sectors three weeks ago, to the Armageddon scenario. And meanwhile the software companies rallied back, as the disruption scenario is now seen as too exaggerated, as we also claimed last week. Technology, previously seen as the under-performer, could now be seen as the “safe-haven”, until this changes again. The “European-renaissance” dream which boosted the regional equities to record highs just one week ago, suddenly became a nightmare from which people want to just rush out. Another exaggeration in the making ? Most probably yes. The worst thing to do is to trade this nausea-causing market. The wise thing to do is perhaps be on the lookout for long-term opportunities that were expensive just a few days ago and they are now getting much more attractive. No one became rich by trying to time the bottom. Many became poor by trying to trade the untradeable.

Make no mistake, this year will probably not be an easy one. Investors should really moderate their expectations compared to the previous years. Whether the lift will take us right back up or we will have to take the stairs is anybody’s guess. The target is to remain in the building and find our way towards a higher floor. Our conviction in the established trends (Technology, Emerging Markets, European renaissance, Consumer spending) remains high, but our deep belief in diversification (defensives, energy, materials etc.) lowers volatility when the world appears to be crashing down. It probably won’t.

Weekly highlights

The February US labor market data caused concern. The non-farm payrolls came in at -92k in February, vs expectations for +55k. Prior months were also revised down, as usual, a cumulative 69k this time. The unemployment rate climbed to 4.4%. Looking in the details the sector that made all the difference was healthcare. It shed 18.6k jobs in the month, against a gain of 116k in January. In fact healthcare had been the support for the labor market for months. Leisure and hospitality were a bit of a macro worry, down 27k and the sector was also down 12k in January.

More news on steep redemptions from private credit funds circulated last week. This time it was one of Blackstone’s large funds which is facing redemptions of about 8bn$, or close to 10% of its total assets. The reason we are following closely these developments is that a credit crunch is the fastest way to ‘destroy money’ and can end bull markets. Nothing screams ‘systemic’ for now as in 2008 but uncertainty in credit can cause a lot of volatility and reprice risk assets lower (in credit an equities) for a few months/quarters. People say that even the collapse of SVB Bank or Credit Suisse were only “hick-ups” for markets, but our response would be that those cases were more about liquidity whereas in private credit, there are increasing signs that solvency is the issue. We are more worried about these events than the Gulf war.

EU February inflation was worse than expected, confirming our view of last week that there was risk of a negative surprise, given the previous week’s data from large individual countries, which came in higher than expected. The EU composite headline number was published at 1.9% vs 1.7% expected, while core CPI moved higher to 2.4%.

Markets’ reaction

Global equities sold off, with Europe being the main victim of a volatile week. The European indices lost 5-7% on average, while the US main indices outperformed as investors rotated back to Technology (Nasdaq -1.2%, Russell 2000 -4%). In terms of sectors, Energy (+1%) was the only positive one but its gains were pared after Monday’s initial big rally. Defensive sectors such as Staples (-4.5%) or Healthcare (-4%) did not provide any cushion as they had rallied before last weekend’s events and valuations had started looking stretched.

The government bond market also sold off, due to the oil price spike. As mentioned last week, a side-effect of the situation is a potential rise in interest rates (yields) as inflation fears could come back. On a positive note, the US yield curve flattened towards the end of the week, which means that the market sold primarily the short-end bonds, pricing out rate cuts by the FED rather than fearing for long-term inflation outlook which would have impacted the long-end even more. Still, the US 10yr finished at 4.20% and the German equivalent touched 2.90% again, a whopping 25bp rise for the week. Yields start looking interesting again in the 4-6yr maturities.

Precious metals fell too, in a week where there was nowhere to hide. After the initial rally on Monday morning, profit taking kicked-in and Gold returned closer to 5100$ while Silver fell by more than 15% from its weekly high. Momentum seems to have been lost for now, as the February sell-off seems to have inflicted pain to traders and they are a lot of losing positions at higher levels, which are being closed down at any attempt for rally. It will take some time for metals to find a sustainable leg higher, as we highlighted a few weeks ago.

The EURUSD fell to 1.1600., as stretched leveraged short positions on the dollar had to be liquidated. Technically, the 1.1500 level appears to be the line on the sand for a capitulation of the shorts. The EURCHF flirted with the 0.8 handle for the first time ever, finishing the week at 0.9010.

Chart of the week:

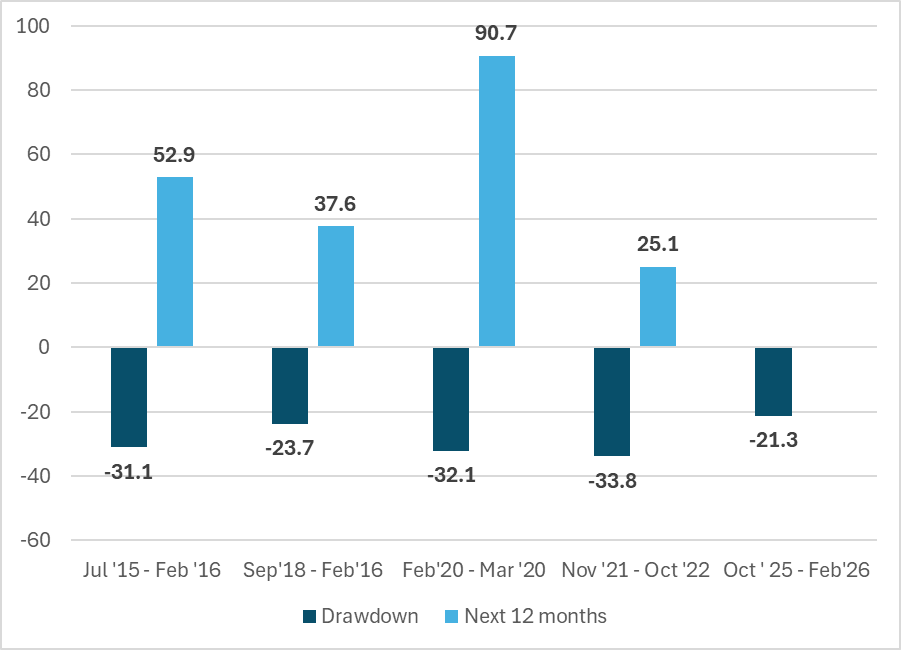

Cybersecurity stocks’ current drawdown calls for potential large rebound.

The above chart shows the price evolution during various similar weak periods for the First Trust Nasdaq Cybersecurity ETF, which contains a basket of global cybersecurity companies. As one can see the current sell off has brought the drawdown since late October to more than 20%, close to previous episodes. One can definitely argue that there is room for further correction especially in the current fragile environment, but according to history such drawdowns are followed by strong returns in the next 12 months. From a fundamental view, we believe that current pricing for some companies represent a great long-term opportunity as the fear for major AI-related disruption appears to be exaggerated. The AI-written code for cybersecurity can’t replace the layered protections offered by traditional cybersecurity tools, including dedicated static analysis, dynamic testing, runtime monitoring and full threat modelling, along with countless other essential safeguarding steps. It seems common sense that enterprise-level companies would never even consider replacing a proven

cybersecurity solution with a ChatGPT generated security script, especially amid the growing complexity and

sophistication of modern cyber-attacks.

Disclaimer

- The content of this document has been produced from publicly available information as well as from internal research and rigorous efforts have been made to verify the accuracy and reasonableness of the hypotheses used. Although unlikely, omissions or errors might however happen.

- The data included in this document are based on past performances and do not constitute an indicator or a guarantee of future performances. Performances are not constant over time and can be positive or negative.

- This document is intended for informational purposes only and should not be construed as an offer or solicitation for the purchase or sale of any financial instrument and it should not be considered as investment advice. The market valuations, views, and calculations contained herein are estimates only and are subject to change without notice. Any investment decision needs to be discussed with your advisor and cannot be based only on this document.

- This document is strictly confidential and should not be distributed further without the explicit consent of Kendra Securities House SA.

- Sources : Chart: KSH/First Trust