Thoughts of the Week

In 1985, one of the top hits globally was the “Money for Nothing” song by Dire Straits. I made the connection when I started thinking by the dire situation at the strait of Hormuz, which has cratered all asset classes and is sending shivers down the governments’, businesses’ and consumers’ spines. In this famous song, manual-labor workers are mocking those in the flashy music business who make millions for doing “nothing”. My brain quickly recreated the image of traders/speculators sitting in their comfortable chairs and making billions of dollars by a few clicks, in the fully computerized oil futures market, which is operating on a 24-hour basis. One has to wonder if the benefits of technology and innovation in financial markets outweigh the danger of having the price of vital commodities for our everyday lives be determined every millisecond by financial derivatives used by speculators.

Prices are supposed to be determined by real supply and demand, and not by the sentiment of traders, which these days, changes by the minute. It was just a few weeks ago that the International Energy Agency (IEA) was forecasting an oversupply of oil for 2026, which means that prices should remain subdued around 60-70$ for Brent (vs. 100$+ now). With its new report out just last week, global oil supply is projected to plunge by 8 mb/day in March, with curtailments in the Middle East partly offset by higher output from non-OPEC+ producers, Kazakhstan and Russia. In the same report, the IEA says that “while the extent of losses will depend on the duration of the conflict and-disruptions to flows, global oil supply will still rise by 1.1 mb/d in 2026 on average, with non-OPEC+ producers accounting for the entire increase“. This means that fundamentally the oil market is still well supplied and prices should eventually come to a much lower equilibrium. And I should mention at this point that oil is a “self-destructing” commodity , as higher prices lead to lower demand (people curtailing activities) and higher supply (producers willing to drill and sell more).

Amidst the panic we also forget that the world is much better prepared now, because of the 2022 events. Governments both in producing and consuming nations have been anticipating such crises. Consumer countries have built huge strategic oil reserves, and this is partly the reason that commodities’ analysts were forecasting low energy prices for 2026 and beyond. Global observed inventories of crude and products are currently assessed at more than 8.2 billion barrels, the highest level since February 2021. Roughly half of these are held in OECD countries, of which 1.25 billion barrels by governments for emergency purposes, with a further 600 million barrels of industry stocks held under government obligation. Well, the reason for accumulating such high strategic reserves maybe has arrived. But producing countries have also taken steps since 2022. Saudi Arabia and the UAE can reroute some crude output to terminals outside the Gulf and have already crude storage arrangements close to consumers.

And Europe does not rely much on Middle Eastern oil, at least not as much as it is being punished for. According to the data, around 80% of the oil products transiting the Strait of Hormuz, and roughly 90% of LNG, are destined for Asia. By contrast, Europe imports only about 4% of its gas, 12% of its oil, and 11% of its LNG from the Middle East. From a narrow physical-delivery perspective, this suggests that Europe is less exposed than Asia, or in other words Europe needs to replace substantially less energy than it did in 2022, when the Russia-Ukraine war triggered a collapse in Russian imports.

Lastly, we still have the view (or the wishful thinking), that taco-Trump will be soon forced to put an end to this, as midterm elections are only eight months away. The first signs of disagreement with Israel’s Netanyahu appeared last week, when the latter said in a press conference that they acted on their own when striking Iran’s very important South Pars oil field. More importantly, he also said that they now have destroyed Iran’s ability to produce nuclear weapons, which means that the main objective of the war has been achieved. Now, if they wish to also bring down the regime, then troops on the ground will have to considered. We believe that this is something that Trump will not agree on, as it will crash his (already slim) chances for maintaining full Congress control in November.

The famous rock band was oracular. Forty year later, money for nothing is indeed easily made and lost in financial markets. We are no oil experts, as we were not epidemiologists back in the days of Covid. As then, we are just trying to calmly evaluate what the markets are pricing-in and whether there are dislocations or in other words, opportunities to accumulate quality assets which are now sold on discount. This is not to say we are naive and underestimate the risks of a full-blown crisis. Then again, the oil price you see on the screens now can be 10% lower or higher with just a click, if you turn your eyes away for a few minutes.

Weekly highlights

The ECB left interest rates unchanged, but the market is now pricing almost 70 bp of rate hikes this year. It was obvious in the press conference that the governing council is really worried about inflationary pressures due to the oil price spike and the money market has responded swiftly. But we believe the ECB will also have to consider the scenario where things could get so disruptive that hiking rates would be a policy mistake, as the economy would be under severe stress. Imagine a situation where the ECB were to hike rates in April or June, only having to reverse them in September. To avoid a U-turn, the ECB might require more time to gain clarity until its next meeting in April, for which the market already applied a 60% chance of a rate hike !

The FED also held rates unchanged, and Chairman Powell tried to strike a balanced note in the press conference. He emphasized several times the dual mandate of the central bank which means that the labor market is equally important as inflation, but when pressed he admitted that rate hikes came up in their discussions on Wednesday. For the moment, the official projections of the committee are for one rate cut this year, but the market as is the case with the EUR, is already pricing higher rates in 2026.

Markets’ reaction

Global equities corrected further. Selling was indiscriminate with US indices finishing down by 2% on average and Europe by 4%, as even Swiss stocks fell by the same magnitude. Asia, despite its large dependence to Iranian oil, managed to behave better, with Japan and Hang Seng dropping less than 1%. In terms of sectors, only Energy was again positive (+3%), whereas even defensive sectors like Staples (-4%) and Utilities (-3%) were under pressure. The Eurostoxx50, Nasdaq and Russell 2000 have now touched the 10% off the recent high level, which is the official definition of a correction. This 10% correction has been often associated with near-term bottoms.

The bond market sell off is reaching a climax. The central bank meetings and the oil price volatility had a major impact on short-term bonds, as yields on 2yr bonds are now discounting rate hikes. The US 2 yr rose to almost 4%, from 3.2% just three weeks ago, while the EUR 2yr touched 2.70%, and as a reminder the ECB rate is at just 2%. Opportunities have arisen again in the 2-3yr high quality bonds, if we assume that the forecasted/feared energy crisis will never come.

Precious metals also crashed. We have often spoken lately about the high correlation of Gold and other metals to equities, that has been in place since speculators discovered them late last year (and derivatives/technology gave them the tools to drive their prices “through the roof”, i.e. same story as with oil these days). We said in mid-February that a wash-out is needed and lessons to be learned, for the market to find a more sustainable equilibrium. Gold returned to 4500$ having lost supports in the 4600-4800$ area and now 4100$ could be in sight, where the 200day moving average resides. Silver fell to 65$, after touching 120$ in late January’s mania and is now negative for the year.

Volatility and panic spread to the foreign exchange market. The EURUSD jumped from 1.1450 to almost 1.1600 on Friday, as the market focused on the prospect of higher rates by the ECB as soon as April. The EURCHF returned to 0.9200, just days after it touched the 0.8 handle.

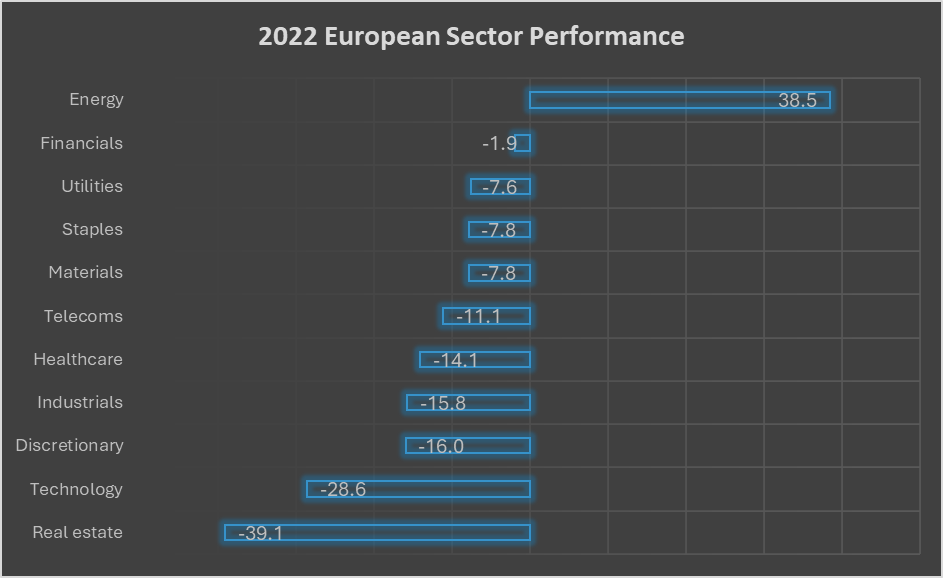

Chart of the week: A 2022 repeat ?

Our central scenario is that 2022 will not be repeated. That was when steep losses were sustained in invested portfolios as both the bond and the equity markets crashed. But it is wise to keep in mind how sectors behaved in Europe which was hit the hardest by the energy crisis and make sure that hedges are in place, just in case the worst case scenario materializes. As the above chart shows, Energy was the best place to be, and we remain well invested in the sector. Surprisingly, Financials also “saved the day” for portfolios , as a steep rise in interest rates is usually beneficial to their profits. However, back in the day the ECB rates rose from zero to 4% and the market came in 2022 as deeply underweight the sector. Things are much different these days and there is also the risk for a blow out in private credit, which makes us very skeptical about this space. Utilities, Staples and Telecoms are boring but helpful and we have them. Lastly we sold any exposure to Real Estate stocks, as it is definitely the sector to be hit the hardest in case of bond yields moving further higher. Technology’s bad performance can be primarily attributed to the burst of the 2020-2021 bubble, as higher interest rates hurt their excessive valuations back then. We have been adding to European Technology during this selloff, as valuations are far less than their bubble years.

Disclaimer

- The content of this document has been produced from publicly available information as well as from internal research and rigorous efforts have been made to verify the accuracy and reasonableness of the hypotheses used. Although unlikely, omissions or errors might however happen.

- The data included in this document are based on past performances and do not constitute an indicator or a guarantee of future performances. Performances are not constant over time and can be positive or negative.

- This document is intended for informational purposes only and should not be construed as an offer or solicitation for the purchase or sale of any financial instrument and it should not be considered as investment advice. The market valuations, views, and calculations contained herein are estimates only and are subject to change without notice. Any investment decision needs to be discussed with your advisor and cannot be based only on this document.

- This document is strictly confidential and should not be distributed further without the explicit consent of Kendra Securities House SA.

- Sources : Chart: KSH / FactSet, Photo: cover of the album “Money for Nothing” by Dire Straits