Thoughts of the Week.

The cover photo is dedicated to Jim Kerr, who is still touring the world. The famous Simple Minds lead singer is still “Alive and Kicking” as he is fast approaching his 70th year. But many would wonder what does this have to do with an investment newsletter, and rightly so. For starters, simple minds (but not simplistic) is one of the pillars of our investment style, avoiding complex investment vehicles and obscure black boxes. “Keeping it simple” has helped us navigate through rough waters many times in the past. And despite all the turmoil of the last three months , the markets are still alive and kicking!

The de-escalating situation in Iran and the AI enthusiasm have been strong catalysts for markets. We had been of the view since the early stages of this military conflict that Trump wants a way out. With an already high probability to lose the House in the midterm elections, he would not risk entering a multi-month war with serious implications for the US economy, which would eventually lead to lose the Senate as well. The evolving situation in the bond market, with the 30yr yield reaching the highest level in four decades at a time when the US government is running high fiscal deficit and debt, must be keeping the US administration up at night.

Although the situation in the Middle East remains extremely fragile, we can assume that we have seen the worst of it, for the next few months at least. Oil prices should eventually stabilize at lower levels, which means that the most affected European sectors such as building materials, cyclicals and consumer-related could outperform in the immediate future. During the sell-off we had increased exposure to companies such as Heidelberg Materials (cement) and more recently KION Group (logistics/forklifts), which are heavily exposed to the “alive and kicking” German infrastructure theme, but had been totally abandoned by investors.

Make no mistake, oil prices should remain elevated vs their pre-war levels for many more months, which means that inflation should remain much higher than the FED’s 2% target for longer. This could have serious implications on the trajectory of US interest rates in the second half of the year, which is perhaps the only catalyst that could “kill” markets.

For now, the AI enthusiasm is keeping investors blind to the risk of higher interest rates. The US retail investor is flocking into leveraged technology ETFs and hot IPOs are coming up. According to reports which surfaced last week, Anthropic, OpenAI and Elon Musk’s SpaceX are preparing their filings for being listed in the stock exchange, as early as the end of summer. These are conditions for the rally to continue, despite hefty valuations in many parts of the Technology sector.

“What you gonna do when things go wrong? What you gonna do when it all cracks up? What you gonna do when the Love burns down? , wondered Jim Kerry in the referenced ’80s song and it is our fiduciary obligation as wealth managers to be asking the same. There are very few hedges that one can put on to avoid a deep correction, as the main catalyst for that appears to be a sharp rise in bond yields. This would also crater the typical safe-havens such as government bonds and gold. The simplest solution is to build positions in sectors that have been left behind in the current frenzy, such as telecoms, healthcare and consumer staples, but with conscious knowledge that these will be severely underperforming if the AI-related party continues unabated.

Weekly highlights

The FED minutes were marginally hawkish, as expected. According to them, “A majority of participants highlighted that some policy firming would likely become appropriate if inflation were to continue to run persistently above 2%”, or in other words rate hikes. As a reminder, FED officials voted last month to hold rates steady, but three Fed presidents objected, not to the rate decision itself but to the wording that retained the so-called easing bias (rate cuts) in the Fed’s statement. That language would have indicated that the Fed’s next move is more likely to be a cut than an increase. The minutes showed that “many” officials would have preferred removing the easing bias, which is a sign of broader voter support than the three formal dissents.

The Bank of America’s May Global Fund Manager survey showed a record rise in equity allocation. Consequently, cash levels fell 0.4 pp to 3.9%, which is the lowest on record. Low cash levels are a potential danger to the rally as there is less fuel to drive it, especially if there is a small correction which could lead fund managers to raise their cash. The Bull & Bear Indicator of the same survey rose to 7.8, just below the 8.0 threshold that indicates sell territory (contrarian indicator).

Eurozone May PMI dropped to 47.6, lower than expected. It was dragged down by Services which dropped to a three year low of 46.5. On the positive side, Manufacturing held up relatively well above the 50 level at 51.4, which confirms our view that infrastructure as well as capital spending for data centers and electrification are still valid investment themes.

Markets’ reaction

Global equities rebounded, with Europe outperforming after several weeks of lackluster returns. The region’s indices rose by 3.0-3.5% , as the S&P500 rose by 0.9%. We had mentioned before that a positive outcome in Iran and a fall in oil prices will turn the focus of investors back to Europe. Technology remained well bid, but semiconductor stocks were volatile after their relentless run.

The bond market recovered too , as oil prices fell. The US 10yr yield dropped to 4.55% after touching 4.70%, while the German equivalent fell to 3.05% after a brief trip to 3.20%. Bundesbank’s Chairman Mr. Nagel said that in the next ECB meeting “they could do something” , hinting that a rate hike will definitely by debated strongly, as the market has already priced in a 25bp rise.

Precious metals were again volatile, and finished on a negative note. Gold has returned to the 4’500$ level and silver ended the week at 75$. Momentum has been lost since the surge at the early part of the year, and it looks probable that the 4’300$ support for Gold could be tested in the next weeks, if the “sell-the-rally” mood persists.

The dollar was stable, with the EURUSD trading around 1.1600 for most of the week. A sustainable solution in the Middle East would probably re-ignite dollar’s downtrend.

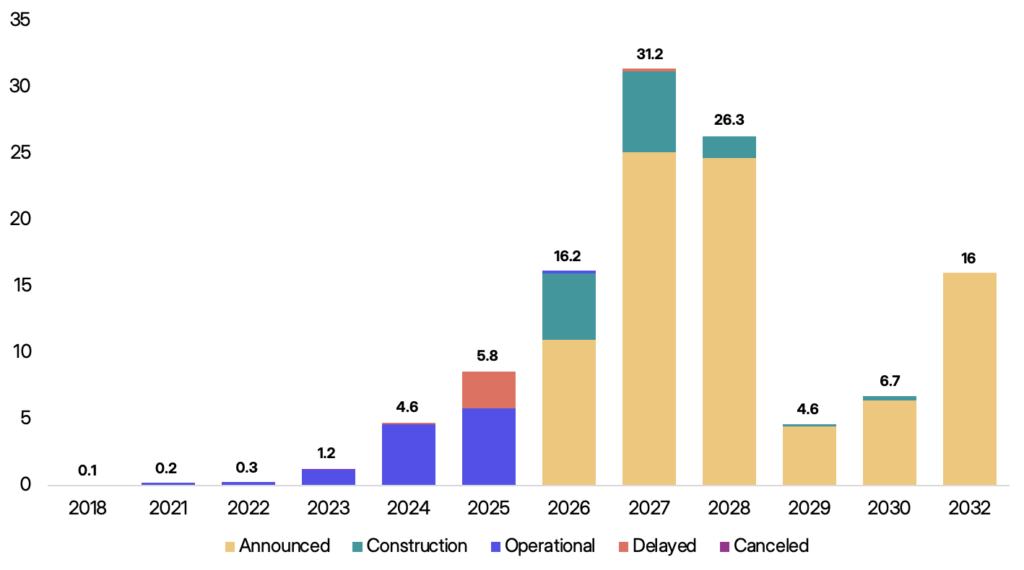

Chart of the week: US Data Centers: Half of the 2026 pipeline might not materialize

An interesting analysis shows that despite the announced capacity for data centers only a fraction is completed. In 2025, 26% of expected capacity slipped, and another 10% of projects pushed back their commercial operation dates without much notice. Although an explosive growth is expected for 2026, perhaps 30–50% of that pipeline is unlikely to come online before the end of the year. The chart is compiled by sightline.com who are tracking 190GW across 777 large data centers and AI factories (>50MW) announced since 2024. At least 16GW of capacity is scheduled to come online in 2026 across roughly 140 projects. Yet only about 5GW is currently under construction. Around 11GW remains in the announced stage with no visible construction progress, despite typical build timelines of 12–18 months. Projected delivery dates are getting harder to trust. Extrapolating the above data, wouldn’t be a surprise if 30–50% of the capacity announced for 2026 ends up delayed. This could have implications for the revenue estimates of the data center beneficiaries for 2026, something that analysts have not incorporated in their forecasts yet.

Sources : Chart: sightlineclimate.com

The content of this document has been produced from publicly available information as well as from internal research and rigorous efforts have been made to verify the accuracy and reasonableness of the hypotheses used. Although unlikely, omissions or errors might however happen.

The data included in this document are based on past performances and do not constitute an indicator or a guarantee of future performances. Performances are not constant over time and can be positive or negative.

This document is intended for informational purposes only and should not be construed as an offer or solicitation for the purchase or sale of any financial instrument and it should not be considered as investment advice. The market valuations, views, and calculations contained herein are estimates only and are subject to change without notice. Any investment decision needs to be discussed with your advisor and cannot be based only on this document.

This document is strictly confidential and should not be distributed further without the explicit consent of Kendra Securities House SA.