Thoughts of the Week.

The 2026 FIFA World Cup starts in just three days ! There are many unique features about this World Cup. It will be the first with 48 teams instead of 32 and the number of matches will jump from 64 to 104. The tournament will last 39 days, up from about 30 during the previous events and it will be the first ever hosted by three countries (United States, Canada, Mexico). This means that there is significantly more content and event time than in past world cups. Small countries such as Cape Verde, Curaçao, Jordan, and Uzbekistan have qualified for the first time ever. And Iran will be taking part in the America-based tournament at a peculiar time …

Between the AI madness and the Iran/Trump saga, the “king of sports” will now catch our attention. Billions of people will make watching a game their daily habit, drinking a Heineken or a Coke alongside a pizza. The more healthy ones would probably chose a Danone yoghurt as dessert when watching the games. Some of them could chose to make cocktails for their friends, perhaps a Margarita with Don Julio Tequila (Diageo), to honor one of the host countries. Millions of people will actually visit the countries that host the event, and will stroll through the various cities spending some time also at the local mall, looking at Tiffany’s jewelry (LVMH) or a Cartier watch (Richemont), buying the official Adidas tournament ball or trying for the first time a pair of ON shoes. Some of them will most probably eat at a McDonald’s, afterwards. And an equally huge number will top-up their accounts with on-line betting platforms to gain a real stake in each game. ( … Italians will most probably chose Lottomatica to place bets against Bosnia that kicked them out of the tournament).

Far from being an influencer, I did mention these sectors and companies for a reason. Major events such as the World Cup have in the past contributed significantly to the revenues of companies in hospitality, travel, luxury, betting and in general the consumer goods and services companies. Although there is no clear statistical correlation between the World Cup and the performance of any of these stocks before or after the event, the fact is that their revenues receive a boost because of it, according to previous earnings reports and comments. What makes this year different is that the tournament comes at a time when revenues of companies in luxury and alcoholic beverages for example, have been dropping for almost three years and they have only recently stabilized. Their shares still sit at multi-year lows with valuations not seen in a decade and a sudden revenue boost could make the difference in the next few months, when they report their Q3 results. Perhaps it is not a coincidence that last week there was a major rotation away from Technology into the consumer-related sectors mentioned in the previous paragraph even if the situation in Iran is still fragile , as these are negatively impacted by higher oil prices.

But what really caused the rotation ? The spike in bond yields that caused the Nasdaq sell-off on Friday was probably just the catalyst. The market had already started questioning the sustainability of the relentless rally of semis and other related companies because there are valid reasons why capital spending on data centers might be at an inflection point. We have already mentioned several times that constraints in building the promised data center capacity could be detrimental for the beneficiaries valuations. First it is the personnel restraints. Moving thousands of people to remote areas where there aren’t enough hotels and restaurants is becoming logistically very difficult. Then there are power generation limitations , an ever-increasing resistance from local habitants and backlash on local politicians ahead of the midterm elections because of surging utility bills. All these have caused delays or cancelations. Back in February a report by Axios highlighted that about one-third of the data-centers planned to be completed in 2025 were already delayed. According to other available data, the 2026 expected capacity will be completed at 50%, at best.

And Anthropic dropped a bomb, saying publicly that top artificial intelligence labs should consider slowing the pace of development. In a blog post published last Thursday, the company claimed that AI systems are advancing so rapidly that they may soon be able to improve themselves without human intervention in ways that could pose significant societal risks. Some AI insiders have seen that threshold as an inflection point and trigger of danger and enormous societal upheaval. Anthropic wrote: “We believe it would be good for the world to have the option to slow or temporarily pause frontier AI development to enable societal structures and alignment research to keep up with the advance of the technology”. And the investment world was left in awe, as the main, if not the only, theme in markets has been explosive data center deployment.

The time for necessary rebalancing has most probably arrived. Last week, we reduced our exposure to Technology after having increased it significantly during the March sell-off. The hype has brought valuations in specific stocks to levels beyond perfection. If earnings upgrades stop because of data center delays or cancelations the related stocks will start falling precipitously. We saw what happened to European defense stocks in the summer of last year when all future growth (NATO 5% spending proposal) was already discounted in the prices and then earnings upgrades stopped and capital moved to other themes. We also thought it would be prudent to take a small step back, because the upcoming enormous Tech IPOs but also the sizable share capital increases (Alphabet, Meta) will temporarily impact liquidity as institutional and other investors will have to sell positions in order to participate. We rotated some capital into beaten-down consumer related names not just of course because of the world cup, but primarily because they either offer defensive growth (Danone) or can significantly outperform when the Iran situation will eventually normalize (BMW, ON Holdings).

Go Nati !!

Weekly highlights

US May non-farm payrolls rose by 172k, smashing estimates of +115k. At the same time, the previous two months were upwardly revised by a total of 93k and unemployment stayed at 4.3%. The data have confirmed the significant improvement of the US labor market in the last few months, which has turned the discussion from rate cuts to rate hikes by the FED, especially now that inflation is far from the 2% target. As a reminder, the FED had turned its attention to the weakening labor market at the end of last year in order to adopt an easing bias (cutting rates) for 2026. Now this is history.

Eurozone inflation rose 0.2pp to 3.2% y/y in line with consensus. As expected, energy rose further by 0.1pp to 10.9% y/y, but less than we expected. Core inflation rose 0.3pp to 2.5%, slightly higher than expected (2.4%) but this increase reflects the reversal of the Easter effect, which raised March inflation (due to its earlier timing compared to last year) and dampened April inflation. Interestingly services inflation rose more than consumer goods while food inflation fell by 0.4pp to 2% y/y. The data are consistent with a rate hike by 25bp when the ECB meets on Thursday.

The US Tech giants are forced to raise capital. Alphabet raised 85bn$ on Wednesday and reports talked that Meta Platforms is coming soon in the market for a similar amount. But this isn’t always good news for shareholders. The once asset-light companies with huge cash flows have become capital-heavy with depleted cash. The recent offerings is yet another sign that the artificial-intelligence ambitions of Big Tech companies are far outstripping their operating cash flows, forcing them to tap debt and equity markets, as was the case in the late 1990s with the telecom companies.

The EU Parliament’s Committee on International Trade approved the trade deal with the US, by 31 votes to 6. The deal was struck in July 2025 in the wake of the US administration’s threats to impose tariffs on imports from the EU. The strong support for the measure in the committee suggests it should also pass when it goes to the EU Parliament plenary later this month. Trump has been complaining and threatening the EU, claiming it was dragging its feet on approving the deal. This development could be another tailwind for the beaten down consumer names.

Markets’ reaction

US equities had their worst week since late March. After a streak of 9 consecutive positive weeks, Nasdaq fell almost 5%, bringing the S&P500 down 2.5%. European equities outperformed, as the sell-off was concentrated in Tech stocks where the US indices are more heavily exposed. The mini rally in consumer names helped the Euro Stoxx50 index to register a small gain (+0.2%) for the week.

The bond market sold off, primarily in the US. After the strong labor market data, the US 2yr yield shot up to 4.20% the highest since last year and about 80bp from the low registered at the end of last year, when the market was expecting 2-3 rate cuts by the FED. The 10yr rose to 4.55% and if the 2yr climbs further to 4.50%, the 10yr will hit the 5% mark, which will spell disaster. The EUR curve also moved higher by 3-4bp across maturities, with the 10yr at 3.05% days before the ECB meeting which will confirm the rate hike already priced-in.

Gold sold off, as yields spiked. As we have said several times, Gold has been in an unfortunate sell-the-rally mode since February and higher interest rates is not the yellow metal’s best friend. It fell to 4350$ down 5% for the week, and perhaps the road is clear for a test of the psychological level 4’000$.

The dollar strengthened as expected. The EURUSD fell close to 1.1500 again as the market has now priced a rate hikes by the FED by December 2026, in stark contrast with the beginning of the year when rate cuts were expected.

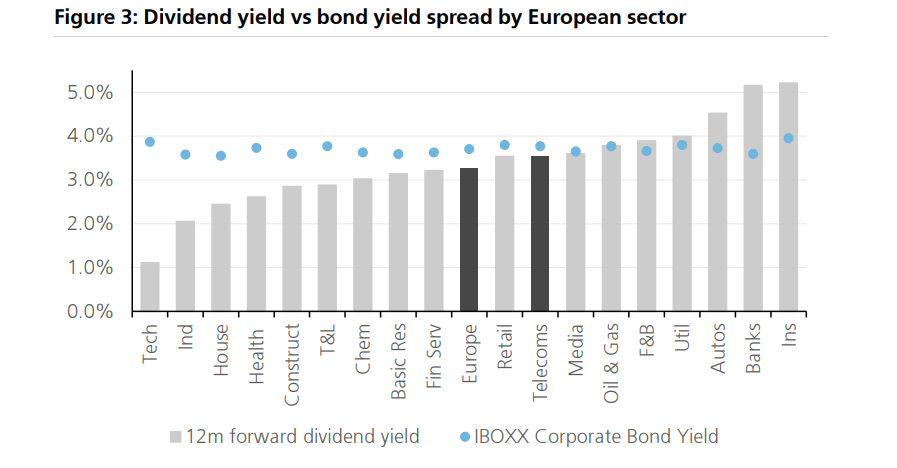

Chart of the week: Where are dividends still attractive ?

Source: UBS

Given the recent rise in corporate bond yields and the rally in some European sectors (hence lower dividend yield) there is now clear competition between the two asset classes for the capital allocation of income oriented investors. The above chart by UBS shows the current average dividend yield for some sectors in grey bars and the corresponding yield of the sector in a blue bullet point. As we can see the recent rally in Industrials (second from left) has brought the dividend yield down to just 2%, whereas the once high-dividend Basic Resources (the likes of Rio Tinto and BHP) is just 3%. The same situation holds with Oil & Gas as the latest big rally in stock prices has caused the dividend yield to drop to less than 4%, equal to the corporate bond yield of the sector. On the far right we see that Autos, Banks and Insurance are still offering decent dividend yields, as their stocks have been left behind during the recent frenzy. For this reason we recently increased positions in Banks and Insurance, and last week we added BMW in the High Income certificate too. Overall, the dividend strategies are getting more complicated and an active approach is needed.

The content of this document has been produced from publicly available information as well as from internal research and rigorous efforts have been made to verify the accuracy and reasonableness of the hypotheses used. Although unlikely, omissions or errors might however happen.

The data included in this document are based on past performances and do not constitute an indicator or a guarantee of future performances. Performances are not constant over time and can be positive or negative.

This document is intended for informational purposes only and should not be construed as an offer or solicitation for the purchase or sale of any financial instrument and it should not be considered as investment advice. The market valuations, views, and calculations contained herein are estimates only and are subject to change without notice. Any investment decision needs to be discussed with your advisor and cannot be based only on this document.

This document is strictly confidential and should not be distributed further without the explicit consent of Kendra Securities House SA.