Thoughts of the week

In football, the half-time break is boring and annoying. After 45 minutes of action, with adrenaline high and emotions flowing according to the score, you have to watch endless commercials , sometimes repeatedly the same. But in our lives, the summer break is always a relief. As you might have already realized this will be our last weekly newsletter until around mid-August.

Instead of commercials, I thought it would be interesting to present the highlights and decisions of our half-year investment committee , which took place last week. In summary:

Markets: Performance dispersion across asset classes stayed elevated. Equity markets remained constructive in the first half of 2026, with World Equities up 11% in dollar terms and Emerging Markets up 26%. Government bonds fell 1%, oil rose 21%, whereas gold declined 7% and Bitcoin fell 33%. In terms of regions, Japan was up 37% and Russell 2000 (+21.7%) outperformed the S&P 500 (+9.5%). Technology was the leading sector in both the US and Europe, with Energy right behind it. AI-capex beneficiary sectors outperformed globally with memory chips having their best quarterly performance on record.

Macro and Interest Rates: The macro environment calls for structurally higher interest rates for longer than anticipated, which poses a risk (the only one at this point) for equities. Western central banks have begun tightening and the FED has a new Chairman with a big question mark on what is in the cards. Uncertainty on the path of FED monetary policy means that yields will remain elevated for now. Eurozone inflation eased back below 3%, with core around 2.4%, while US inflation rose to 4.2% headline and 2.8% core, much higher than the 2% target.

Equities: Earnings expectations continue to improve, with 2026 EPS growth now estimated at approximately 23% for the S&P 500 and 18% for STOXX Europe 600. However, concentration risk has increased materially, with technology approaching 40% of the S&P 500, semiconductors at 20% of the index, and leverage is high, with US margin lending close to $1.5 trillion, up 54% year on year. This supports a lower-beta exposure in the short term and more selective equity stance. Europe has started outperforming again the US since early June. A new oil price spike will, of course, dent this trend. Emerging Markets are vulnerable to rotation, as just three semiconductor stocks (Samsung, Hynix, TSMC) are now 30% of the index.

In Equity portfolios we have concluded that AI will remain a core investment theme. But at this stage it is better to favor lagging Technology, such as Software (Microsoft, SAP). The recent weakness has also provided a good entry point for power generation beneficiaries (Siemens Energy). And we have started diversifying portfolios, by taking advantage of the de-rating in certain sectors and adding positions in Quality Growth (EssilorLuxottica) as well as Value (Munich Re, Swiss Re, JPMorgan, BMW). Given the fragile situation in the Middle East and the view that oil prices will remain elevated, Energy exposure must be maintained. Active funds are preferred for exposure in Emerging Markets, with our main position being in Value-tilted strategies, to reduce reliance on the concentration risk mentioned above.

For our fixed income exposure we maintain low duration. We continue to favor flexible bond funds as the preferred core allocation. Government bonds and longer duration act mainly as hedges in a severe recession or credit-crunch scenario, which for now are not likely outcomes. Actually, the long duration bonds appear to be a negative catalyst for equity markets at this stage, and hence portfolios could suffer a double-whammy effect.

I take the opportunity to wish you a peaceful and enjoyable summer , while assuring you that the “break” is not really a break, but rather a change of location. Our internal company structure as well as technical infrastructure guarantee that markets are continuously followed and corrective actions in portfolios can take place regardless.

Weekly highlights

The minutes of the FED’s meeting did not provide any new information. They showed that the committee is deeply divided between those wishing rates to stay at current or lower levels and those who would like them to be at current or higher levels by year end. Kevin Warsh will have a very difficult task to make the case for lower rates given elevated inflation, improved labor market and AI’s tailwind to the US economy. His main point will be that AI will boost productivity, which by itself is a deflationary force, but this is not enough to convince the majority of voting members to push the button for rate cuts.

Kevin Warsh announced the first five “big-shots” for his task forces. Among the names , the most prominent are ex-BoE Chairman Mervyn King and the ex Governor of Central Bank of India Raghuram Rajan. And perhaps the most controversial is that of venture capitalist billionaire and crypto-maniac Marc Andreessen. The task forces are going to examine areas central to the broad conduct of monetary policy: Communications (how it conveys policy deliberations and decisions), Balance Sheet Policy (costs, benefits, and institutional implications of the current balance sheet regime, Data (improve the quality and timeliness of real economic signals), Productivity and Jobs (assess the economic impact of new general-purpose technologies, including artificial intelligence) and Inflation Frameworks (revisit how the FED understands and responds to the drivers of inflation).

The Q2 earnings season is starting, first in the US. In the next three weeks we will have most of the important S&P500 companies reporting , starting with the major financials this week. The big Tech will follow in the second half of the month, while in Europe, ASML will report next week. As already mentioned July will be a hot month, in any direction, but seasonality is positive.

Markets’ reaction

Global equities had mixed performance, last week. The new exchange of airstrikes between Iran and the US caused a correction in European equities, with its main indices down about 2%. At the same time the rebound in beaten-down memory stocks pushed the S&P500 higher by 1.2%. On the contrary the Russell 2000 and the Dow Jones finished lower. In terms of sectors, investors chose to sell the defensives (staples, healthcare) to focus again on Technology, but Energy had a come back after the spike in oil prices.

The bond market moved lower. The US 10yr yield rose closer to 4.60% and the 2yr is back above 4.20%. In the Eurozone, yields also moved higher, with the 10yr German bund approaching 3.10%, a whopping 20bp spike in just a few days.

Gold fell as yields rose. The yellow metal fell closer to 4’050$ again confirming the difficult technical backdrop, where mini-rallies are still being sold. On the positive side, the 4k level appears to be well supported for now, as Asia demand is reportedly picking up around those levels.

The dollar did not move much. The EURUSD has been stuck for now in a tight range around 1.1450.

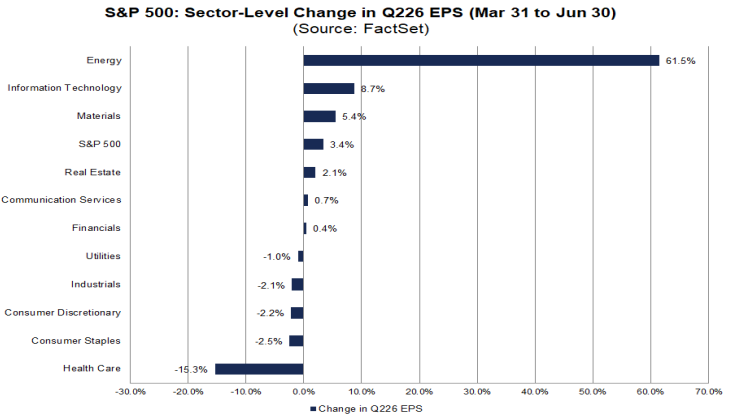

Chart of the week: How earnings estimates have changed in the last 3 months.

Source: FactSet

As of today, the S&P 500 is expected to report (year-over-year) earnings growth of 23.3%, compared to the estimated (year-over-year) earnings growth rate of 18.8% on March 31. This is due to the upward revisions to earnings estimates by analysts and the positive EPS guidance issued by companies. The above chart shows the level of revisions of expected profits per sector. As you can see Energy has seen its expected profits increase by more than 60% in the previous few months, due to the spike in oil prices. The second largest upward revision has been, as expected, in Technology (+8.7%). Four sectors have been revised downwards with the biggest decline in Healthcare. From an investment perspective higher expectations means that stocks have performed well during this period of the upgrades but also higher risk for disappointment, whereas lower expectations has led to weaker share prices and always carry the potential for positive surprises. Still, for our portfolios we always prefer companies with rising earnings estimates, even if that means that share prices are prone for short-term disappointment, after the results.

The content of this document has been produced from publicly available information as well as from internal research and rigorous efforts have been made to verify the accuracy and reasonableness of the hypotheses used. Although unlikely, omissions or errors might however happen.

The data included in this document are based on past performances and do not constitute an indicator or a guarantee of future performances. Performances are not constant over time and can be positive or negative.

This document is intended for informational purposes only and should not be construed as an offer or solicitation for the purchase or sale of any financial instrument and it should not be considered as investment advice. The market valuations, views, and calculations contained herein are estimates only and are subject to change without notice. Any investment decision needs to be discussed with your advisor and cannot be based only on this document.

This document is strictly confidential and should not be distributed further without the explicit consent of Kendra Securities House SA.