Thoughts of the week

Listening to FED Chairman Kevin Warsh’s press conference, the famous Alan Greenspan came to my mind. For those who do not know, he was the King of the FED for twenty years (1987-2006). This is not a surprise though. Mr. Warsh has repeatedly invoked Greenspan as his role model, including at his swearing-in ceremony and earlier as nominee. “I’ve known five of my predecessors in this job, some of them quite well. But Chairman Greenspan was the first to tell me and show me what this role demands. Like Alan, I intend to fill the role of chairman with energy and purpose“, were his exact words. Treasury Secretary Mr. Bessent, who favored Warsh to be the Chairman, also frequently cites Greenspan as a historical model for managing the US economy. Last but note least, Warsh’s swearing-in ceremony took place at the White House, which is a rare event. Alan Greenspan was the last Chairman to have been sworn-in at the same location …

For those of us involved in financial markets during the wild late ’90s, our days started with whether Alan Greenspan said anything. Among other famous instances, in December ’96 he talked about “irrational exuberance” referring to overvalued equities, and the market ignored him and continued to surge with the S&P doubling through 1999. Then the FED raised interest rates by 150 bps between mid‑1999 and May 2000 and we all know what happened next. Interestingly, just before the crash of 2000, Professor Shiller had published a book called “Irrational Exuberance” to remind Greenspan’s quote. Following the three year bear market and the subsequent recession, the FED slashed interest rates to a record low of 1% in 2003 and stayed there for years. This cheap credit flooded the market, making mortgages easily accessible and drove a massive boom in housing prices. At the same time, he actively opposed the regulation of derivatives, such as mortgage-backed securities (MBS) and credit default swaps. This created an environment where banks and financial institutions were emboldened to take excessive risks and create complex financial products, leading up to the 2008 financial crisis. Greenspan has been partly blamed for that.

Déjà vu. The new “Greenspan”, Kevin Warsh is now at the helm of the world’s most significant central bank. The first thing that he promised is to change the FED communications approach. He said that the related task force would consider changes to press conferences, dot plans, meetings, transcripts, minutes etc. We can safely assume that markets will quickly have to adjust to an absence of the so-called forward guidance, which has been in place for the last twenty years or so. Before that, one of Wall Street’s most closely watched indicators was Alan Greenspan’s briefcase. As cameras caught the Fed chairman walking into the Eccles Building before FED meetings, traders scrutinized the thickness of the leather case, betting that a “fat” briefcase meant a policy move was coming. The famous “briefcase indicator” never had real statistical power, but it shows how desperate we all were to find a clue of what comes next in terms of interest rates. Kevin Warsh sent a message that the “briefcase” is coming back (perhaps a laptop or iPad this time).

Sweeping changes are coming with potential significant market implications. Chairman Warsh informed the public that he has already created five task forces, which will be responsible to implement changes where necessary. In fact, he used the words “task force” 29 times in his press conference. Apart from the communications changes already mentioned above, these task forces will review the “benefits and risks of the current ample reserves regime and the composition of the Fed’s balance sheet“, they will evaluate new information sources and consider methodological changes to improve data gathering, they will survey the economic impact of new technologies (AI) and finally they will examine the drivers of inflation and weigh the full range of ideas for delivering price stability in a changing economy. Or in other words, a total rebuild of the FED.

Markets will now dive into the unknown. For almost twenty years , equity markets knew that the FED will always step-in to save a falling market as well as provide them necessary forward guidance as to what the central banks’ intentions were. Most importantly, Kevin Warsh has always been a critic of the ballooning balance sheet, the result of almost continuous quantitative easing (printing money) since 2008 and especially since the pandemic. The printing money machine was there to provide ample liquidity, which is the fuel for asset prices (bonds and equities) to move constantly higher. The majority of today’s traders and fund managers do not have live experience of anything else than this beautiful environment. And this could be about to change.

The markets reacted strongly, which could be a sign of how the next months can evolve. Equities sold off, although they partly recovered the following day, while the dollar rallied as yields rose to now price-in a rate hike as early as October. This is a 180-degree turn from what the rate environment was at the beginning of the year, when two or three rate cuts were expected. A few weeks ago the cover story of our newsletter was “when the doves cry” , explaining that there is a hawkish turn at the FED with regard to rates and warned about its implications. This is now becoming a market consensus, after the FED meeting last week. Add to that the nervousness about the new Chairman, the potential abolishment of forward guidance as well as a willingness to lower the balance sheet (i.e. less liquidity) and there is a high probability that rates will move higher and stay there longer. US equities are not prepared for that, but for now they only care about data centers and memory chips. We are preparing for a volatile summer with interest rates as a potential negative catalyst and hence we have increased defensiveness in portfolios, “hiding” in boring stocks that nobody wants to hold (for now).

Weekly highlights

The FED held rates unchanged, as expected. The press conference appeared to be more hawkish than the market was expecting, with the clear message that the focus is now inflation, as the labor market has stabilized and improved since the end of the year.

The Swiss National Bank left the policy rate unchanged at 0%, as expected. In the statement, the SNB added the words “if necessary” in the sentence “The SNB will continue to monitor the situation and adjust its monetary policy if necessary, in order to ensure price stability.” This could be interpreted as a downscaling of the bank’s willingness to intervene, but it could also be signaling to the market that since their last meeting in March the SNB has only intervened during times of stress, i.e. when it was “necessary” and not on a continuous basis. Hence the central bank is not ultra-anxious about the currency’s strength at current levels, but it would not want it to strengthen abruptly either. From an investment point view, it confirms the view that the Swiss Franc is on a secular multi-year uptrend against most currencies, albeit at a gradual pace.

The US and Iran have reached a fragile deal. If it was not for the serious implications on the world, this would have been characterized as a joke. Trump signed the ceasefire agreement in Versailles, France but the situation is changing on a daily basis, primarily because there are still hostilities in Lebanon between Israeli forces and Hezbollah, which for Iran has been a red line for the final deal. The US-Israel relationship is currently strained as Trump and Netanyahu have obviously very different agendas and nobody knows what the endgame will look like. For the moment, the Hormuz strait is still essentially closed and global oil reserves are running dangerously low.

Markets’ reaction

Global equities continued their rebound. As the Iran situation seems to be gradually normalizing and oil prices fell more than 20%, equities recovered further. The S&P500 added 1%, as Technology (+2.5%) was strong, albeit volatile. Eurozone equities outperformed with a 1.7% gain for the week, also helped by the momentum trades (Technology, Industrials) as Energy (-7%) was under pressure on both sides of the Atlantic. Defensive sectors were also not in fashion as investors jumped back to the this year’s winners, with Healthcare and Staples down 2-3% for the week. A great time to pick up some of these names again.

The bond market was volatile. The initial euphoria due to the steep drop in oil prices was quickly followed by a sell-off in USD government bonds, after the FED meeting and Warsh’s press conference. The US 2yr yield rose to 4.20% and the 10yr traded closer to 4.50% again. The EUR yields did not move much and the 10yr Bund remained below 3%.

Gold took a dive , together with the other precious metals. The rise in yields and the dollar rally are not Gold’s best friends and hence it dropped to around 4’150 again, failing to rebound further towards its 200-day moving average.

The dollar rallied, as mentioned above. The EURUSD fell close 1.1400, as traders cut their short bets on the USD.

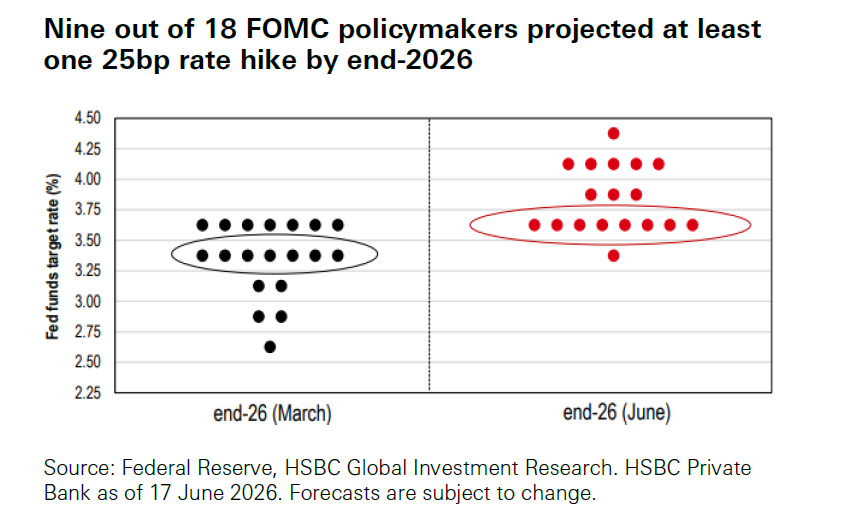

Chart of the week: What a difference three months make …

Source: KSH/FactSet

The above chart is the famous FED dot plot that shows where each member of the Federal Open Market Committee (FOMC) believes the federal funds interest rate should be in the future. Each policymaker’s projection is represented by a single dot. The dots are provided by the 7 members of the Board of Governors and the 12 regional Federal Reserve Bank presidents. Although 19 members in total provide their forecast, only 12 of them vote at each meeting. The 7 members of the Board of Governors always vote for monetary policy, but only 5 of 12 regional presidents vote, in turns which change on a yearly basis. As we can see in the chart the dots have moved significantly higher since end of March with half of the participants now forecasting a rate hike, until end of 2026. The red ellipse shows the members who believe that rates will stay on hold until year end, and there is only one who believes rates will be cut. And most of the 9 who see rate hikes, forecast more than one ! Interestingly, Mr. Warsh did not provide his own dot, a symbolic move and message to the public that this procedure a) is not very reliable as they keep changing their minds, which of course is normal as circumstances change and b) will be under review to be changed or cancelled altogether.

The content of this document has been produced from publicly available information as well as from internal research and rigorous efforts have been made to verify the accuracy and reasonableness of the hypotheses used. Although unlikely, omissions or errors might however happen.

The data included in this document are based on past performances and do not constitute an indicator or a guarantee of future performances. Performances are not constant over time and can be positive or negative.

This document is intended for informational purposes only and should not be construed as an offer or solicitation for the purchase or sale of any financial instrument and it should not be considered as investment advice. The market valuations, views, and calculations contained herein are estimates only and are subject to change without notice. Any investment decision needs to be discussed with your advisor and cannot be based only on this document.

This document is strictly confidential and should not be distributed further without the explicit consent of Kendra Securities House SA.